How to calculate impairment on intercompany loans?

“I work for a group and we have a lot of intercompany loans. I read your article on ifrsbox about this topic and you mentioned that we have to book impairment on intercompany loans.

How shall we do it? What should we consider?”

Answer: Apply ECL model.

This is a very broad question, but I’m glad you asked.

In the past, when IAS 39 was applicable, many groups or companies ignored impairment or let’s call it more friendly – a loan loss provision to intragroup loans.

Why?

The reason is that under IAS 39, you need to apply the incurred impairment loss model, or in other words, you booked the impairment once it has already incurred, without estimating what you expect to loose in the future.

Under IFRS 9, this is no longer true.

You have to apply expected credit loss model and here, you actually estimate what you will lose in the future on top of what you have already lost.

And, you need to book the loan loss provision in the amount of expected credit loss.

Now you might ask – why bother if at consolidation, all the loan with provision would be eliminated?

Yes, that’s true, but if the loan is provided to the parent by the subsidiary, then the impairment of this loan will bring the subsidiary’s profit down and as a result, the parent’s dividend would be lower than without any impairment – so please think of it.

There is so many considerations that I can’t really cover them all in one podcast episode, but I will try to give you some hints and maybe I’ll write some article about it later.

So first, I’m going to explain how you should calculate the expected credit loss and then, I’ll outline a few points to consider especially for intercompany loans.

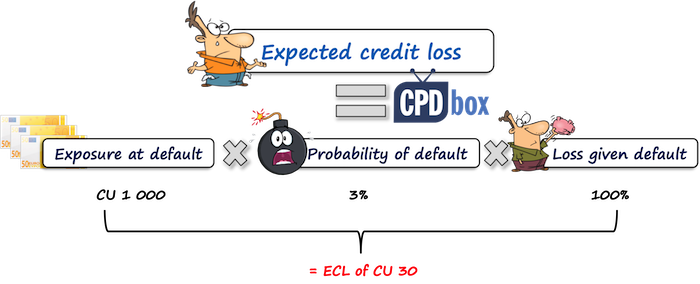

What is expected credit loss (ECL)?

It is the weighted average of credit lossess with the respective risks of defaults occurring as the weights.

Here, we have three elements to include:

- Exposure at default (EAD) is the total amount of the loan outstanding, so it’s how much one company owes to another company at the reporting date;

- Probability of default – it is the percentage and it is the likelihood that the borrower will not be able to repay its debt within some period;

- Loss given default – it is also the percentage and it is how much the lender loses if the borrower defaults and is not able to repay its debts.

Let’s say that the loan outstanding is 1 000, the probability that the borrower defaults is 3% and in this case the lender would lose the full amount of the loan – so the loss given default is 100%.

The expected credit loss is exposure at default of 1 000, multiplied with probability of default of 3% multiplied with loss given default of 100% = so, the impairment or the expected credit loss is 30.

Troubles with impairment on intercompany loans

It all might be theoretically clear, but there are a few difficulties with intercompany loans, for example:

- For intercompany loans, you need to apply general 3-stage model, not simplified model.It means you have to assess at which stage the loan is first and then perform calculations.I wrote an article about it here and also, my premium course the IFRS Kit contains really nice explanations and illustrations of this model, so please check that out if interested.

- It is difficult to get inputs to calculations: loss given at default and probability of default, because intercompany loans are usually not credit rated.I mean, you can have the credit rating of the external loans with banks and you would derive the probability of default based on that rating, but not with internal loans.Special For You! Have you already checked out the IFRS Kit ? It’s a full IFRS learning package with more than 40 hours of private video tutorials, more than 140 IFRS case studies solved in Excel, more than 180 pages of handouts and many bonuses included. If you take action today and subscribe to the IFRS Kit, you’ll get it at discount! Click here to check it out!

And, you cannot apply external rating to internal loan without any adjustment, because the internal and external loans are not equal – you usually pay your external debtors first, and only then to your mom.

So, what should you do?

Useful tips to determine the impairment loss on intercompany loans

Is it a loan?

Look to the terms of a loan first.

It can happen that it is not a loan at all, but some capital contribution by the parent or a distribution from the subsidiary if we have the opposite direction.

I write more about it in this article and if this is the case, then it’s not a loan under IFRS 9 and you can forget about the impairment.

OK, let’s say it is a loan.

Is the loan repayable on demand?

Many intercompany loans are deemed as repayable on demand. In other words, the lender can just ask the borrower – send me the money back.

In this case, the question is:

Does the borrower have enough cash to repay the loan immediately?

- If yes, then there is no impairment, or the impairment is probably not material and you can forget about it.

- If not, then the lender should make some calculations of the potential impairment, for example, the lender should estimate the probable repayment calendar and discount the cash flows to the present value.

Determine the stage of the loan

If the loan is not repayable on demand, then we need to determine at what stage it is.

The reason is that if the loan is in stage 1 – that is, a performing or healthy asset, then you should calculate impairment

at 12-month ECL.

It means that you need to estimate the probability of default within the next 12 months .

I think that in most cases, your impairment would be close to zero or immaterial because if it’s a healthy asset, then the probability of default is very low. But you should test it.

If the loan is at stage 2 or 3 – so, if the credit risk has significantly increased or the loan has already defaulted, you need to calculate the impairment at life-time ECL.

So, you need to take the probability of default within the whole loan’s life into account which might be quite demanding to determine.

How to set the probability of default for intercompany loan?

Well, it’s not easy and it requires some work.

For example, you should take a look to the history of repayment of intercompany loans by the borrower.

Or, maybe your group is so advanced that it produces its own internal ratings.

Or, maybe you can use the external credit ratings of the companies within the same industry and make adjustment based on how the borrower performs currently.

Don’t forget to incorporate the forward looking information – in this article I give you some direction of how to do it.

Also, remember, except for probability of default, you need to set the loss given default – or how much the lender will lose if the borrower defaults.

What factors can affect the loss given default?

Things like guarantees and collaterals usually decrease the loss given default, because they give at least something back to the lender in case of borrower’s default.

Let me mention one specialty with intercompany loans.

Parent company can provide a letter of support to the subsidiary stating that in case of default, the parent company will send enough cash or otherwise support the subsidiary to cope with the situation.

Yes, you can take that into account when estimating your loss given default, but usually letters of support are not that strong as guarantees with third parties or collaterals and often they have limited validity.

I can continue talking about the impairment of intragroup loans, but my aim was just to give you the overview of what’s on the agenda and perhaps I will write long article or make some video in the future.

Anyway, if you have some question or comment, feel free to add it below – thank you!

[powerpress] [addtoany]JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

1 Comment

Leave a Reply

Dear Silvia,

Did I understand correctly that in consolidation (considering your example) elimination of IC Loan will be done by the following eje:

Dr Loan received 100

Cr Loan given 70

Cr ECL 30

?

Thank you.