Example: How to Consolidate

Let’s be more practical today and learn some advanced accounting techniques.

After summaries of standards related to consolidation and group accounts, I’d like to show you how to prepare consolidated financial statements step by step.

I’ll do it on a case study, with explaining what I do and why. If you don’t like reading, you can skip to the end of this article and watch my video.

If you’d like to revise a theory first, then please read my summary of IFRS 3 Business Combinations and IFRS 10 Consolidated Financial Statements, both of them contain video in the end.

What’s the situation?

Here’s the question:

Mommy Corp has owned 80% shares of Baby Ltd since Baby’s incorporation.

Below there are statements of financial positions of both Mommy and Baby at 31 December 20X4.

Prepare consolidated statement of financial position of Mommy Group as at 31 December 20X4. Measure NCI at its proportionate share of Baby’s net assets.

Please note here that in the above statements of financial position, all assets are with “+” and all liabilities are with “-“. I use it this way because for me it’s easier to verify and identify mistakes, but it’s up to you.

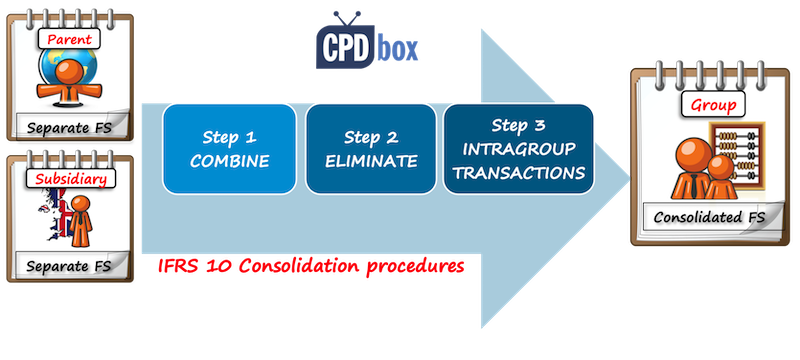

3 Steps in Consolidation Procedures

I have described the consolidation procedures and their 3-step process in my previous article with the summary of IFRS 10 Consolidated financial statements, but let me repeat it here and follow these steps:

- Combine like items of assets, liabilities, equity, income, expenses and cash flows of the parent with those of its subsidiaries;

- Offset (eliminate):

- the carrying amount of the parent’s investment in each subsidiary; and

- the parent’s portion of equity of each subsidiary;

- Eliminate in full intragroup assets and liabilities, equity, income, expenses and cash flows relating to transactions between entities of the group.

Step 1: Combine

After you make sure that all subsidiary’s assets and liabilities are stated at fair values and all the other conditions are met, you can combine, or add up like items.

It’s very easy when a parent (Mommy) and a subsidiary (Baby) use the same format of the statement of financial position – you just add Mommy’s PPE and Baby’s PPE, Mommy’s cash and Baby’s cash balance, etc.

In reality, companies use their own format for presenting their financial position and therefore it can be difficult to combine. That’s exactly WHY so many groups use their “consolidation packages” and subsidiaries’ accountants must fill them up along with preparing own financial statements.

Therefore, when a group controller calls you every five minutes to remind you the consolidation package, you’ll know why!

In our case study, combined numbers looks as follows:

Of course, there are some strange and redundant numbers, for example both Mommy’s and Baby’s share capital, but we haven’t finished yet!

Step 2: Eliminate

After combining like items, we need to offset (eliminate):

- the carrying amount of the parent’s investment in each subsidiary; and

- the parent’s portion of equity of each subsidiary;

and of course, recognize any non-controlling interest and goodwill.

So let’s proceed. The first two items are easy – just remove Mommy’s investment into Baby (CU – 70 000), and remove Baby’s share capital in full (CU + 80 000).

As there is some non-controlling interest of 20% (please see below), you need to remove its share in Baby’s post-acquisition retained earnings of CU 9 000 (20%*CU 45 000).

Wait a second – how do we know that all Baby’s reserves (retained earnings) of CU 45 000 are post-acquisition?

Well, the question says that Mommy has owned Baby’s shares since its incorporation, therefore full Baby’s retained earnings are post-acquisition.

Be careful here, because you absolutely need to differentiate pre-acquisition retained earnings from post-acquisition retained earnings, but here, we’re not going to complicate the things.

Then we need to recognize any non-controlling interest and goodwill.

Non-controlling interest at 31 December 20X4

Mommy has owned 80% of Baby’s share and therefore, non-controlling interest owns remaining 20% of Baby’s net assets.

The question asks to measure non-controlling interest at proportionate share on Baby’s net assets, so here’s how it looks like at the end of the reporting period:

Baby’s net assets are CU 125 000 as at 31 December 20X4, including Baby’s share capital of CU 80 000 and Baby’s post-acquisition reserves of CU 45 000.

Non-controlling interest at 31 December 20X4 is 20% of Baby’s net assets of CU 125 000, which is CU 25 000. Recognize it with minus, as we are crediting equity with non-controlling interest.

Initial recognition of goodwill

There might be some goodwill arisen on initial recognition. If you’d like to learn more about goodwill, please refer to the article about IFRS 3 Business Combinations.

Let’s calculate it. Please don’t forget that we calculate goodwill based on numbers on acquisition, not on 31 December 20X4.

The goodwill is calculated as:

- Fair value of consideration transferred: in this case, we simply take Mommy’s investment in Baby of CU 70 000;

- Add any non-controlling interest at acquisition: here, we’re not adding the non-controlling interest calculated above, as it’s the measurement on 31 December 20X4. At acquisition, the value of non-controlling interest is 20% of Baby’s net assets on its incorporation of CU 80 000 (share capital only). It equals CU 16 000.

- When a business combination was achieved in stages, you would need to add the acquisition-date fair value of the acquirer’s previously-held equity interest in the acquiree, but in this example, it’s not applicable,

- Deduct Baby’s net assets at acquisition: CU – 80 000.

Goodwill acquired in a business combination comes to CU 6 000 (70 000 + 16 000 – 80 000).

The elimination entry looks as follows (sign “+” indicates a debit entry; sign “-“ indicates a credit entry):

| Description | Amount | Debit | Credit |

| Remove Mommy’s investment in Baby | -70 000 | FP – Investment in Baby | |

| Remove Baby’s share capital in full | +80 000 | FP – Baby’s share capital | |

| Remove 20% (NCI) of Baby’s post-acquisition retained earnings | +9 000 | FP – Retained earnings | |

| Recognize non-controlling interest on 31 December 20X4 | -25 000 | FP – Non-controlling interest | |

| Recognize goodwill acquired in a business combination | +6 000 | FP – Intangible assets (goodwill) | |

| Check | 0 |

I have transferred this journal entry into our consolidation worksheet and it looks as follows:

Eliminate Intragroup Transactions

Parents and subsidiaries trade with each other very often.

However, when you look at both parent and subsidiary as at 1 company, which is the purpose of consolidation, then you find out that there’s no transaction at all.

In other words, group has not performed any transaction from the view of some external user.

Therefore you need to eliminate all transactions happening within the group, between a parent and its subsidiaries.

Looking to above individual statements of financial position of Mommy and Baby you see that Mommy has a receivable to Baby of CU 8 000 and Baby has a payable to Mommy of CU 8 000. Perhaps these 2 items relate to the same transaction between them and we need to eliminate them, by debiting payables and crediting receivables:

Final steps

After we have completed all steps or consolidation procedures, we can add up all the combined numbers with our adjustments and thus we arrive at consolidated statement of financial position.

You can revise all the steps and formulas in Excel file that you can download at the end of this article.

Here’s how it looks like:

Please note the following facts:

- Consolidated numbers are simply sum of Mommy’s balance, Baby’s balance and all adjustments or entries (Steps 1-3).

- Mommy’s investment in Baby’s shares is 0 as we eliminated it in the step 2. The same applies for Baby’s share capital and consolidated statement of financial position shows only a share capital of Mommy (parent).

- There’s a goodwill of CU 6 000 and non-controlling interest of CU 25 000, as we have calculated above.

- Consolidated retained earnings are CU 98 000 and they consist of:

- Mommy’s retained earnings of CU 62 000 in full, and

- Mommy’s share (80%) on Baby’s post-acquisition retained earnings of CU 45 000, that is CU 36 000

Exam-style consolidation

I know that many of you prepare for your exams and this is NOT the way how you learned consolidation during exam preparation courses.

OK, I understand.

I prefer this way of making consolidation by far, because here, you go systematically, step by step. You can deal with each adjustment in a separate column and as a result, your numbers will always balance. You will never forget anything.

The “exam-style” of making consolidated financial statements is good and easy when there are just a few issues or complications.

But when you need to deal with more complex situations, then you can forget or omit the things very easily. Trust me, I did it too.

However, to make you happy, you can find the same case study solved “by the exam-style” in the attached excel file that you can download in the end of this article.

Is consolidation really easy?

Sometimes.

But in most cases, there is lots of issues or circumstances that you need to take into account and exactly their significance and amount makes it all difficult.

What issues? For example:

- Consideration transferred for acquiring the shares may involve not only cash, but also some other forms, such as share issue, contingent consideration, transfers of assets, etc.

- Non-controlling interest can be measured at fair value instead of at proportionate share.

- There might be some unrealized profit on transactions within the group and it needs to be eliminated.

- There might be some transfer of property, plant and equipment at profit within the group and as a result, you need to adjust both unrealized profit and depreciation charge, too.

- Goodwill might be either positive or negative (=gain on a bargain purchase). Moreover, it can be impaired.

- Subsidiary’s net assets might be stated in the amounts different from their fair value, or even not recognized at all.

- Subsidiary may show both pre-acquisition retained earnings and post-acquisition retained earnings. You need to be extremely careful in differentiating them and dealing with them separately.

I can go on and on, but I don’t want to discourage you. However, if you need to know more about all these issues, I have covered them fully in my premium learning package the IFRS Kit, so please check out if interested.

Please watch the video here:

Further reading: Here’s the example of consolidation where a subsidiary has different functional currency than its parent. You’ll learn how to translate the subsidiary’s financial statements.

Here, you can learn the opposite process – disposal of subsidiary (deconsolidation).

If you like this example and explanations, please help me spread a word about it and share it with your friends. Thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

227 Comments

Leave a Reply

Hi Silvia, thanks for the insightful article. I have question on how to attribute post-acquisition profit to NCI where a shareholders’ agreement exists that modifies the profit entitlement of the subsidiary’s shareholders. Lets consider an example of a 60% owned subsidiary and the agreement between its shareholders’ provides the following:

1. The 40% share capital to be contributed by the other shareholders (hereafter referred to as “NCI”) shall be paid up by the parent company (who is the 60% shareholder) in form of advancement to NCI.

2. The advancement shall be repaid to the holding company by way of setting off against future dividend to be distributed to NCI.

In the absence of the above factors, the consolidated income statements of the parent company should report the profit attributable to the parent company and NCI based on their respective ownership interest. This would result in attributing CU 40 to NCI if the current year profit of the subsidiary is CU 100.

However, having the additional factors in mind, if the advancement owed by NCI is CU 40, and should there be any dividend distribution in the future, NCI will never get paid for the CU40 profit attributed to them because the payment will instead be diverted to the holding company to settle the advancement they owe. In that sense, should the CU 40 profit be attributed to NCI at the first place?

Hi Silvia

When we need to adjust the Subsidiary net assets to fair value – do we do revaluation entries in the consolidate statements ?

For example, if we need to recognise client lists or provisions that wouldn’t be in the individual statements – do we debit assets client lists and credit p&l

Or debit PPE – credit revaluation reserve ?

What about the provisions for probable liabilities ?

Hi Daniel, you do all adjustments when consolidating, but in the separate statements. If you are subscribed to our courses, there’s a full solved example about it.

How to account for the pre – acquisition deficit in an asset acquisition? In a business combination, this would be accounted when calculating goodwill.

You can read and watch the video about it here.

Thank you!

What is the difference between GAAP and IFRS when considering consolidation to GAAP financials in the US.

Basically they are completely different sets of accounting and reporting rules. Please see more here.

Hi Silvia

If I have company A which has associate B and B has subsidairy C 100%

Now Company A wants to acquire full C

What the impact in books of Company A and Company B

I just wanted to thank you for this amazing, wonderful and extraordinary work you do for us students. You really make IFRS more digest. you are a STAR!

Thanks Silvia. Helpful.

Few requests, pl..

1)Step 2: Eliminate – removing Baby’s share capital in full ,ie.CU 80 000. Could we remove only 64000, ie. the parent’s portion of Baby’s equity instead?

2)Removal of 20% NCI of Baby’s post-acquisition retained earnings: Why is this required, pl.?

Hi Selva- What is the possible case, that a dividends from subsidiaries are shown on the consolidated statement of cash flow only ?!

Hi Silvia, I have a question on consolidation and I hope that you can share your opinion on this problem.

The background of the case was as follows:

Company A asked its directors to set up a company (Company B) in Country X in the 1980s. The shares in Company B are registered under the individual directors name. Company B operates independently from Company A and there was no information whether Company A has control over Company B.

In 2020, the new management of Company A sued the former directors and claimed that the shares held by them in Company B are in trust for Company A. In 2021, Company A won the suit and the Court passed a judgment saying that Company A is the rightful owner of the shares in Company B. The Court also ordered the former directors to pay Company A legal costs and all the dividends (plus interest) they received from Company B in those years. In 2022, the shares in Company B are successfully transferred to Company A and Company B become a wholly owned subsidiary of Company A.

My questions are:

(a) Is this a prior year adjustment? Can Company A recognise Company B as subsidiary in 2022 on the basis that Company A does not have control over B until the shares have been transferred?

(b) If Company A recognised Company B as subsidiary in 2022, what is the “cost of investments” amount to be recorded in A books? Is it legal fees incurred by Company A or the share capital of Company B?

(c) How does Company A record the compensation received (past dividends, interest and legal costs) from the former directors?

(d) How does the above transactions recorded in the Group level?

Thank you for your help.

Kelvin

Thank you Silvia for your illustration ,

If you don’t mind I have two questions regarding the consolidation, the first one why we eliminate the retained earnings that exits at the acquisition date (or before the acquisition date) ? is it like the amount that it’s hidden for the future that the investor will take it from the investee ? the second question when we eliminate intragroup transactions regarding purchasing of PPE or Inventory : if the sale is made from the parent to its subsidiary why we do not reduce the subsidiary share for unrealized profit since the subsidiary will take part of the net Assets (equity) that are attributable to (non-controlling interest)? in other words if the net assets affected for the group the net assets for the non-controlling interest will be affected also.

Thank you in advance.

Regards,

Mohammad Obeid

1. Because they enter in the goodwill calculation and do not belong to the group as they were achieved prior acquisition date.

2. Because the parent made unrealized profit, not the subsidiary, in your outlined transaction.

Mohammed, I strongly recommend you to look inside the IFRS Kit, because these questions are all solved there.

Thank you for your response and advice,

In reference to answer No. 2 , in your videos when the Subsidiary made sale to its parent you allocate the amount of unrealized profit also to Controlling interest(parent share in Retained Earnings , 80% of the total amount) although the amount of unrealized profit should reflect the non-controlling interest.

Thanks in advance.

And that is correct. However in your question, you asked about the opposite situation.

yes but your answer is ” Because the parent made unrealized profit, not the subsidiary” regarding the reason of not allocating part of unrealized profit to non-controlling interest despite we calculate the percentage of unrealized profit to controlling interest in the case when the subsidiary made a sale to its parent.

Thank you for your Answer,

Regarding answer No.1 if this is the case then all Assets and Liabilities that are acquired by the parent at the acquisition date are not belong to that investor because the Investee who assume these Assets and Liabilities, it’s like the retained earnings that achieved prior to the acquisition date right ?

No. Please see more in the IFRS Kit.

Thank you Silvia for your illustration,

I have a question about the elimination for “related party” transactions, can we say that the reason of not including these transactions in the consolidated Financial Statements is these transactions are not between Arm’s length transactions and therefore it does not reflect the Commercial substance of the transaction since one party has control over another? For example the transfer pricing between the parent and subsidiary in different countries its just transfer the retained earnings or “Capital” from one country to another to avoid the taxation.

Thank you in advance.

Regards

Mohammad Obeid

No. The reason for not including them in consolidated financial statements has nothing to do with commercial substance. They are included because if we treat the group as one entity, then these transactions are between “individual departments” within the same entity, so from the outside view, there are no transactions.

Hi Silvia,

How do we consolidate if the acquisition date happened in the middle of the year?

Hi jan, basically you consolidate balance sheet in full and profit or loss only since the acquisition date until the end of the reporting period. Profit or loss items incurred from the beginning of the period til the acquisition date are considered pre-acquisition and enter into calculation of goodwill and NCI. I cover it quite well with practical examples in the IFRS Kit, so please check that out if interested.

Hi Silvia,

An individual is a shareholder in both parent and subsidiary companies. Will his interest be added to the interest held by the parent company in determining the minority interest in a subsidiary company? Thanks

Hi Silvia,

Thank you very much for the good work, We can leisurely learn and love to read the content.

You can reshape people by sharing your knowledge.

I want to pay for IFRS kit, how do I do it? In Uganda

Please write me via Contact form. Thank you!

if there are intercompany sales. is the minority interest calculated based on the eliminated net income.for eg if the standlone net income of the subsidiary is 20,000 after elimination it is 15,000. then minority interest share of earnings will be 15000 multiplied by ownership % of minority interest?

Ok Silva i know that the Consolidation one of the several difficult techniques independently makes a difference ….. what is the other techniques from your Opinion would you talk to us about it

thank you too much for all you Do for us here

Hi Sylvia and everyone else,

Hope you all are doing well,

Can you please shed some light on my below questions regarding the presentation of Accounts ?

My question is that if we have audited the Interim accounts for the period ended 31-Dec-2020 and we have purchased a subsidiary in this particular period only (before this period, Parent had no subsidiary ), so, do we have to show unconsolidated accounts or not, for the 30-June-2020 period end (for Balance sheet) to show it as comparative Accounts ?

And for PnL, to show comparative accounts for 31-Dec-2019, do we have to consolidate it or not in order to present it as comparative accounts for 31-Dec-2020 period end audit.

Thanks. Simplify a quite involving process.

Hi Sylvia,

Thanks for this article.

Just a follow up question, will there be any change if baby( the subsidiary) should have share premium in her book.

Hi Silvia just looked at your youtube video and have subscribed, im currently confused as to what method i should use and how to calculate NCI at % of net assets and at Full Fair value, would you be able to assist me and tell me which method would be better and why? Again it will be different depending on the depending GAAP but lets just say UK

Expander plc wishes to acquire a 70% stake in Target plc by purchasing 280 million of Target’s 400

million £1 ordinary shares. Target currently has retained earnings of £1,360 million and is not

expecting to issue any shares or pay any dividends in the immediate future. The purchase of Target

will be paid for through a combination of immediate and deferred cash payments.

Expander will pay £5,000 million of cash at the date of acquisition, plus a further £2,000 million in

two years’ time.

Target has some valuable brands, trade names and internet domain names. These are not currently

recognised in Target’s financial statements. The estimated fair value of these assets is £3,500 million

and these brands and domain names are estimated to have a useful life of approximately 8 years.

Expander has not yet determined whether it should measure non-controlling interest in its

subsidiaries on the basis of a proportionate interest in the identifiable net assets of the subsidiary or

whether it should use the “full goodwill” method. The fair value of a 30% holding in Target is

estimated to be £2,500 million.

Where appropriate you may assume a discount rate of 5% per annum.

What does mean by “subsuming intangible assets in goodwill”?

Hello,

Why does the subsidiary share capital remain the same at acquisition and at balance sheet date ?

and why do we show parent’s share capital only, in consolidated financials?

waiting for your reply thank you

Dear Silvia, Thank you for the great article.

May I ask a question on revaluation please? If a parent company revalue its investment in subsidiary and recognize a surplus, then how I can eliminate or offset the carrying amount of the parent’s investment in subsidiary(which is revalued); and the parent’s portion of equity of each subsidiary(which is unchanged). Would you please guide me?

Thank you.

HI. SILVIA, X company purchased 960000 million shares from other one a few years ago. At the time subsidiary had $190 million in reserves. The fair value of non – controlling interest at the date of acquisition was $330 million. How can i work out group structure, % of parent share

Hi Silvia, baby company sold the goods to mommy company at DAP price; therefore the freight cost should be bear by baby company.

In consolidation level, baby company sales = mommy company cost of good sold; should baby company need to report the freight cost for consolidation? the freight cost is paid by baby company to outside forwarder.

how do you calculate legal/statutory reserve at the consolidated level.

hie SILVIA I AM FINDING IT DIFFICULT TO WORK CONSOLIDATION QUESTION OF A GROUP WITH TWO SUBSIDIARIES HOW CAN I DO IT

How would I calculate Goodwill if NCI is measured at Fair Value

Good day

i would like to know what happens when the group sells an asset outside,how do we recognize the transaction? second uestion,when the inventory must be eliminated and there is the net realizable value used, what should i do?

Hello, great tutorial. However, how would you adjust these figures if there were some pre-acquisition earnings to apportion out?

Hi Silvia,

Thanks greatly for your very helpful explanation, I do have a situation where one of our companies had completed the acquisition of 70% of CS equity of another company on December 31, 2019, so do I still need to do the consolidated financials for the year 2019 based on this scenario ?

Thanks very much.

hi Sivlia!

what has to haapen if the parent and subsidiary have different reporting dates?

Hi Silvia!

One question: Why don’t you incorporate fair values in the consolidated?

Simplicity is the key. This is a basic example to teach the basic technique. For more advanced examples, there’s IFRS Kit.

Please need explanation on this.

If a company previously become an associate of the parent entity, parent entity owned less than 50%, later become a subsidiary, the ownership shares increased, how would I put the entries to recognize as a subsidiary from an associate in consolidation?

Hi Douglas, please read this article.

Hi Silvia,

If a subsidiary is at loss position, will the NCI be written down to negative value? Or zero is the bottom for the loss absorption by NCI?

Many thanks

Alice

Yes, negative value.

Thank you very much Silvia!

Hi silva

i just need you help to ward the direct business combination acquisition cost. When cash is paid for different direct acquisition related types the assets of the combiner business specially cash account is affected. But, my question which capital accounts of combiner business parallel affected. Because, IFRS 3 stated that the acquirer shall account for acquisition-related costs as expenses in the periods in which the costs are incurred and the services are received,

Debit-expense & Credit cash…..

Hi Silvia,

I have this below question that really hope to get your help with: the Mother Co sold some shares of its Son Co to NCI. The shares were issued at a higher price so the capital $$ received is higher than the percentage of holdings given. Illustrated like below:

Share Capital $800 total, Son Co 600 and NCI 200, but holding percentage Son Co 80% and NCI 20%

So on console elimination the above all eliminated by $$.

The current year (assume all post acquisition) retained earnings $100. If portion between Mother group and NCI by holding percentage it would be $80/$20, but if portion by $amount injected then it would be $75/25.

For verification the total assets are $900 (800 + 100), portion by percentage of holding it would be $720/180. It doesn’t support either above elimination computation results for NCI: i.e.

1/ $200 + $20 = $220, or

2/ $200 + 25 = $225

So what I did wrong?

Desperately waiting for your reply.

Many thanks!

Alice

Dear Alice, I would like to recommend you our online advisory service – our consultants can answer exactly to these highly specific questions within 2 business days. S.

and by the way it’s the Son Co sold 18% of holdings to NCI for 180, so no goodwill for Son Co or Grandpa Co, I think.

Many thanks

Alice

Hi Silvia, if the intermediate holding company (Son Co) doesn’t provide consolidation because the utmost holding entity (Grandpa Co) provide the consolidation, would 1) the Grandson Co be consoled first with Son Co and then Son Co console with Grandpa Co, or 2) Grandpa Co console directly with both Son Co and Grandson Co, i.e. Son and Grandson be treated like two individual and parallel entities in the Grandpa Co’s consolidation? And if it’s the 2) situation how the intragroup elimination should be provided?

Many thanks

Hi Alice, I would say the option 2 is more probable 🙂 Of course, if Grandpa fully controls both companies, then all intragroup balances need to be eliminated in full. Well, I will write an article about complex consolidation soon!

Thank you Silvia!

Yet a further question: if the Son Co and Grandson Co are both foreign currency entity, say, Singapore Dollar. Son invest SGD1000 into Grandson Co.

Grandpa Co is USD (the group’s console report currency), for consolidation what exchange rate should be used for the Son’s investment of SGD1000 in Grandson Co? for 1st, 2nd, 3rd… years?

Many thanks

Alice

Alice, for all currency questions, I recommend reading this article. S.

Thanks Silvia. I did read that articles multiple times… maybe I should post the question under that article?

My question is the different currency is NOT between the ultimate holding Co (the console entity), but between the two subsidiaries of it that are both the same foreign currency.

Anyways, I posted another question that I desperately needed answer on, but it disappeared? I’ll post again.

Many thanks

Alice

Hi there, I am not sure if I am asking this question on the correct platform, but this is bothering me a bit in terms of consolidation. What do you do if a Trust has the majority Shareholding? Let’s say they have control and it is not an Investment entity. How does it work exactly? Will the trust present Financial Statements? And what will your consolidation look like?

Hi Charne, the first question is: is the trust following IFRS? Is the trust presenting its financial statements under IFRS? This is the question and the answer depends on the legislation of the trust’s jurisdiction and trust’s intentions (if voluntary application is selected) – not on IFRS. If the answer is yes, then in most cases the trust is not exempted from consolidation – but it also depends on the specific structure of the trust.

Hi Silvia,

Your explanation is so good!

Could you please explain why Mommy has invested 70k only but the Share capital of Baby becomes 80k?

Well, it seems that Mommy did not buy 100% share in Baby 🙂

Hi Silvia,

Thanks for the nice presentation.

During the consolidation of my subsidiaries and parent company A/C, i face below problem and want your kind support.. Let The the parent company is “X” and there are two subsidiaries “Y” & “Z” and X holding 99.5% share of Y & Z, and also Y holding 1 % share of Z. Now I am confused how can i eliminate the investment of Y in Z share during the consolidation.

thank u

Hi,

good presentation.

Interested to receive updates regarding this.

thank you,

Hi Silvia,

This is a good article.

i would like to more and more.

Regards

Mohamed Fouad

Hi Silvia,

Query on alignment of Accounting Policies under IFRS Consolidated Financial Statements:

Let say both parent and subsidiary had invested in unlisted / unquoted security of Co. A

If parent determined the fair value of such security using income approach at CU 100 and for the same security in Co. A subsidiary determines fair value using market approach at CU 130.

Is alignment required in consolidated financial statement? Or can this be allowed on the basis that fair value is an accounting estimate?

Requesting some clarity in such scenario.

Thanks

I really appreciate what you are doing to us I personally benefited a lot from this article thank you