IFRS 15 Examples: How IFRS 15 Affects Your Company

IFRS 15 Contracts with Customers introduced a huge change and a very difficult challenge for almost every single company.

After I wrote a couple of articles about IFRS 15 here and here, and after I discussed with some of my friends CFOs or auditors, there are two types of reactions:

- Either people feel that this is A CHALLENGE and they ask me how IFRS 15 can possibly affect them; OR

- People even don’t realize this is a challenge and as a result, they do literally nothing in order to prepare themselves. As we say – sweet ignorance. Or as English says: ignorance is a bliss.

Please, be the exception and stand out from the crowd.

Be aware of what IFRS 15 and its implementation can mean for your company and prepare early enough.

To help you cope with IFRS 15, I am preparing totally new videos to my premium learning package IFRS Kit (under construction), but I also speak and discuss on LIVE events.

I also wrote this article for you to give you a few IFRS 15 examples and hints – all with the purpose to warn you.

This is probably the longest article I have ever published (about 5 000 words and it took me about 30 hours to write it), but you don’t have to read it all, although I do recommend it as you will find a lot of analogy for your own situation.

Believe me, here, we are just skimming the surface and there’s a lot more to analyze, assess, plan and implement.

Now let’s start.

What industries will be the most affected?

For some companies, the impact of the new rules for revenue recognition will be minimal and they will simply continue recognizing revenue just as before. No headaches.

However, some companies might face difficult challenges in order to apply the new rules. The biggest challenges will be mainly in the areas that are not very precisely arranged by IAS 18 and other related standards.

As opposed to existing guidance, IFRS 15 gives you much less room for your own accounting decisions and specifies a lot more things.

The biggest areas of impact are probably:

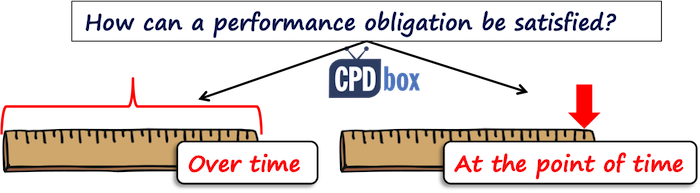

- Is the revenue recognized over time (spread between the periods during contract duration) or at the point of time (upon completion)?

- If the revenue is to be recognized over time, how should the company measure the progress towards completion (previously “stage of completion”)?

- How shall companies account for revenue from bundled offers (with multiple deliverables)? Should they split the contract into several components?

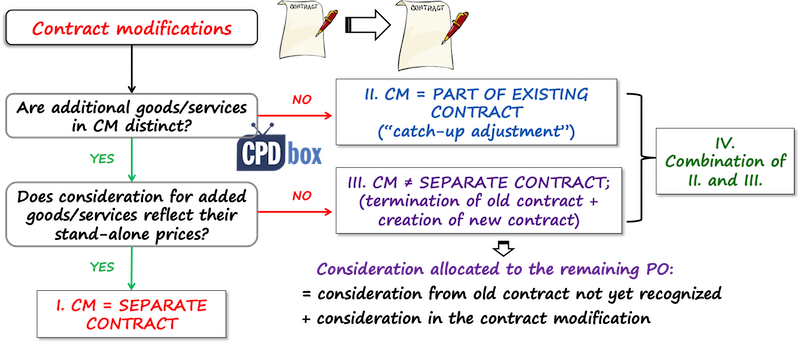

- How shall companies deal with contract modifications?

- How shall companies treat the contract costs, including cost of obtaining the contract? Shall they expense these costs in profit or loss, or capitalize and defer?

- Are there any financing components in the contract? If yes, how to deal with the time value of money?

- What disclosures do companies need to make? Do they have all the appropriate and relevant information?

Different sectors or industries are affected in many different ways along the 5-step model. Here, I selected 4 important industries that will face probably the biggest challenges:

- Telecommunications (with link to example: Identifying individual performance obligations and allocating transaction price)

- Manufacturers (example included below: Contract modifications)

- Real estate and property development (example included below: Revenue over time/at the point of time)

- Software development and technology (example included below: Splitting the contract into 2 separate obligations)

Little disclaimer: It is really impossible to write about everything here as that would be enough to write a book. Analyzed sectors can face different challenges too. And if you don’t find your sector here, just go through these 4 as there’s a lot of analogy.

#1 Telecommunications

Therefore, the main challenge will be to split bundled offers into individual performance obligations and allocate the transaction price.

Also, the revenue for the individual performance obligations might be recognized over time (e.g. 2 years subscription plan), or at the point of time (e.g. delivery of handset).

Short example of a similar situation:

Under IAS 18, many telecom operators provided free handsets to customers and treated them as “marketing costs”, or costs to obtain a client.

Under IFRS 15, this is not permitted, as IFRS 15 requires allocating the transaction price to individual performance obligations.

In this case, telecom operators must allocate total contract price between the revenue from the sale of handset and sale of monthly plan.

As a result, the timing of revenue recognition changes, because under IFRS 15, the revenue is recognized earlier than under IAS 18. I have already written an article with the specific example of this situation, so please refer here.

Another implication of this treatment is that the revenue recognition does not correspond with monthly billing to customers, as there will be some deferral accounts involved.

This is really challenging because implementation will require significant changes in the IT systems, so that IT systems can automatically calculate and book the amount of revenue recognized each month.

Further challenges in telecom industry are:

- Contract modifications:

what happens when customers modify their contracts with operators, for example – change the amount of prepaid minutes or add new services?Here, it will be necessary to assess whether such a change shall be accounted for retrospectively (one-off adjustment) or prospectively (as a “catch-up” adjustment to future revenues), or even as for a separate contract. As IFRS 15 contains more precise rules than IAS 18, it can trigger the change in the accounting systems.

- Time value of money and discounting:

IFRS 15 strictly defines the “financing component” and requires accounting for such a component separately from revenue.As a result, maybe you would need to carefully incorporate time value of money into some long-term advances received or paid, or contracts settled after more than 12 months.

- Costs related to obtaining a customer:

Any industry, not only telecom industry, pays so-called “success fees” or commissions for obtaining a client. Before, these costs were normally expensed and recognized in profit or loss.However, IFRS 15 requires capitalizing them and recognizing them in profit or loss in line with revenue recognition. How are telecom operators going to do that? What will be the pattern of expensing these costs in P/L?

Example: Telecom and individual performance obligations: please refer here.

#2 Manufacturer Companies

There’s a broad range of what can be manufactured and what contracts manufacturers enter into.

If you manufacture similar items in large amounts that are basically typified and not too specific, then you can still be affected by IFRS 15 – just look to example below.

However, manufacturers of specific equipment or goods in general with long period of a production can be affected painfully.

What you should watch out:

- Should you recognize revenue over time or at the point of time? If over time, how are you going to measure the progress towards completion?

- How should you account for contract modifications, e.g. for delivering additional items of goods?

- Do you provide post-delivery rebates? Volume discounts? Year-end bonuses to customers based on total volume ordered during the year? Then you are probably affected by IFRS 15.

- Should you split your contract into more performance obligations? This could be the case when you provide some warranty period for your products – should the warranty be accounted for separately? Are you providing any other services for your products?

- Do you incur certain costs for obtaining the contract, like bonuses to sales team? Maybe you should capitalize them, and not expense them immediately as before.

To illustrate the potential impact of IFRS 15, let me give you one example dealing with contract modification. In this case, we’ll take a look at subsequent order for the same goods with the same customer.

Example: Manufacturers and contract modifications

Ball PC, computer manufacturer, enters into contract with Forward University to deliver 300 computers for total price of CU 600 000 (CU 2 000 per computer).

Due to necessary preparation works, Forward University agrees to deliver computers in 3 separate deliveries during the forthcoming 3 months (100 computers in each delivery). Forward University takes control over the computers at delivery.

After the first delivery is made, Forward University and Ball PC amend the contract. Ball PC will supply 200 additional computers (500 in total).

How should Ball PC account for the revenue from this contract for the year ended 31 December 20X1 if:

- Scenario 1: The price for additional 200 computers was agreed at CU 388 000, being CU 1 940 per computer. Ball PC provided a volume discount of 3% for additional delivery which reflects the normal volume discounts provided in similar contracts with other customers.

- Scenario 2: The price for additional 200 computers was agreed at CU 280 000, being CU 1 400 per computer. Ball PC provided a discount of 30% for additional delivery because it hopes for the future cooperation with Forward University (nothing even discussed yet).

As of 31 December 20X1, Ball PC delivered 400 computers (300 as agreed initially and 100 under the contract amendment).

Revenue under previous rules (IAS 18)

Well, here, nothing much to say. By definition of revenue in line with IAS 18, the revenue for the delivery is simply accounted at the time of delivery, in the fair value of consideration received for the computers – which is whatever amount under 2 above scenarios.

You are not required by IAS 18 to examine whether this additional delivery reflects stand-alone selling prices or not. Also, let’s not complicate the things with issues such as “commercial substance”, “transfer pricing”, “dumping prices” – this is just an example.

The revenue for the year ended 31 December 20X1:

- Scenario 1: CU 600 000 (the first 300 computers) + CU 194 000 (additional 100 computers delivered) = CU 794 000 (for all 400 computers already delivered).

- Scenario 2: CU 600 000 (the first 300 computers) + CU 140 000 (additional 100 computers) = CU 740 000 (for all 400 computers already delivered)

Is it the same under IFRS 15?

You bet it is NOT!

Revenue under IFRS 15

Here, the additional contract represents typical contract modification, as the amount of computers changes and the total transaction price changes, too.

IFRS 15 precisely specifies how to account for contract modifications, based on the terms of modification. There are 2 basic types of contract modification:

- Contract modification is a separate contract

Contract modification is accounted for as for a separate contract (meaning that the original contract is left as it is), when 2 criteria are fulfilled:

- Additional goods and services in the modification must be distinct from the goods or services in the original contract.

In both scenarios, this is met, as additional computers are quite distinct from the original computers.

- Amount of consideration expected for the additional goods/services must reflect the stand-alone selling price of these goods/services.

- Additional goods and services in the modification must be distinct from the goods or services in the original contract.

- Contract modification is not a separate contract

If the above criteria are not fulfilled (or one of them is not met), then the contract modification is not a separate contract and the accounting depends on further analysis.

Let’s take a look at our situation. Here, as we concluded that additional goods are distinct, the main question is whether the additional consideration reflects their stand-alone selling prices.

Scenario 1: 3% discount agreed on additional delivery

The price for additional computers indeed reflects their stand-alone selling prices, because Ball PC normally provides 3% volume discount.

Therefore, this contract modification is accounted for as a separate contract and revenue for the year 20X1 (400 computers delivered) is:

- CU 600 000 from the original contract for 300 computers;

CU 194 000 from the contract modification for additional 100 computers delivered.

Total revenue in the year 20X1 is therefore CU 794 000 – exactly as under IAS 18.

Scenario 2: 30% discount agreed on additional delivery

Here, it’s clear that the price for additional computers does not reflect their stand-alone selling prices, because 30% discount is exceptional and tied to the overall contract with the Forward University.

It means that the second criterion is not met.

As a result, the contract modification is NOT a separate contract, but it is bundled with the original contract.

How?

In this case, as additional goods are distinct, you need to account as you would terminate the original contract and start the new one.

Still unclear?

You simply recognize the revenue from the delivery already made before contract modification under the original contract.

For the remaining goods from the original contract and additional goods, you recognize total revenue amounting to:

- That part of consideration in the original contract that hasn’t been recognized as revenue yet (in other words, price for goods yet to be delivered); PLUS

- The consideration agreed in the contract modification.

You need to allocate this amount to individual performance obligations, or individual computers in this case.

In the scenario 2, contract modification was made after the first delivery, so Ball PC needs to recognize revenue for the first 100 computers in line with the original contract:

100 computers x CU 2 000 per computer = CU 200 000

Total transaction price to allocate after the contract modification is:

- CU 400 000, being the part of original consideration related to undelivered 200 computers (300 per contract less 100 delivered; times 2 000 per unit);

- CU 280 000, being total consideration for additional 200 computers;

- Total: CU 680 000

We need to allocate CU 680 000 to 400 computers in total (200 undelivered before contract modification + 200 additional computers), which means that Ball PC allocates CU 1 700 to one computer (680 000/400).

So what’s the total revenue recognized in 20X1 during which 400 computers were delivered? Let’s calculate:

- Revenue for 100 computers delivered before contract modification: CU 200 000 (CU 2 000/computer)

- Revenue for 300 computers delivered after contract modification: CU 510 000 (CU 1 700/computer);

- Total: CU 710 000.

Here you can clearly see that in this second scenario (additional delivery with 30% discount):

- Under IAS 18, revenue for the year 20X1 is CU 740 000.

The revenue to be recognized in the next period is remaining 100 computers at CU 1 400 = 140 000; that gives us total CU 880 000 per contract. - Under IFRS 15, revenue for the year 20X1 is CU 710 000.

The revenue to be recognized in the next period is remaining 100 computers at CU 1 700 = 170 000; that gives us total CU 880 000 per contract.

Hmm, but the totals are the same!

Yes, sure. But the timing of revenue is different. And exactly this timing can impact your taxes, dividends, financial rations and everything. Just think it out carefully!

#3 Real Estate – Construction Companies and Property Developers

The biggest challenge is to decide whether the company should recognize revenue over time (spread during individual years of construction) or at the point of time (one-time at the completion of a contract).

IFRS 15 lists 3 situations when an entity needs to recognize revenue over time:

For property developers and construction companies, especially one situation is crucial:

When the entity’s performance does not create an asset with alternative use to the entity and the entity has an enforceable right to payment for performance completed to date, then the revenue is recognized over time.

For example, when a company constructs or develops an asset so specific for the customer that it would be very costly or impracticable to transfer to other customer (e.g. building with highly customized specification). At the same time, customer is obliged to pay for work completed to date in the reasonable amount.

Alternatively, “no alternative use” can be achieved contractually, meaning that the contract prevents directing the asset to another customer.

For real estate companies it will be crucial to assess whether the property developer has an enforceable right to payment for performance completed to date or not.

This is not the only criterion to decide, but it is prevailing for real estate.

If the specific contract does not meet this criterion (and also the other two), then the revenue is recognized at the point of time; that is, when an asset is delivered to customer.

Only slight change in the provisions of the specific contract may trigger the necessity to recognize revenue at the point of time rather than over time – or vice versa.

Let’s take a look at the example illustrating exactly this point.

Example: Property developer and revenue over time/at the point of time

RE Construct, property developer, builds a residential complex consisting of 50 apartments. Apartments have a similar size and proportions – however, they can be customized to clients’ needs.

RE Construct enters into 2 contracts with 2 different clients (A and B). Both clients want to buy almost identical apartments and agree with total price of CU 100 000 per apartment. The payment schedule is as follows:

- Upon the signature of a contract, clients pay deposit of CU 10 000 each.

- Milestone: 1 year prior planned completion, RE Construct will deliver progress reports to clients and clients need to pay CU 50 000 each.

- Completion: Upon the completion of the construction, the legal ownership to apartments is transferred to clients and they pay the remaining amount of CU 40 000 each.

Assumed period of construction is 2 years from the date of contract. RE Construct has the right to retain the payments from any client in the situation when that client defaults on the contract before its completion.

The contracts with clients A and B are NOT identical. Further contractual terms specify that:

- No other specific terms in the contract with client A.

- The contract with client B specifies that RE Construct cannot transfer or direct the apartment to another client and in return, the client B cannot terminate the contract.

If the client B defaults on the contract before its completion (in other words, does not make payments in line with the schedule), RE Construct has the right for all contractual price if RE Construct decides to complete the contract.

What’s the difference here?

In the case of client A, the revenue would be recognized at the point of time and revenue from contract B over time.

Why?

We need to assess 3 criteria for recognizing revenue over time. As I have mentioned above, we will not deal with the first 2 here (let’s say they are not met), but let’s focus on the third criterion (no alternative use and enforceable right to payments).

Revenue from contract with client A – at the point of time

The contract with client A does NOT meet the third criterion.

The reason is that RE Construct builds an apartment that can be easily sold or transferred to another client in case of default.

Even when this would be prevented (by writing specifically in the contract), RE Construct has NO enforceable right to payment for performance completed to date.

RE Construct will keep ONLY the progress payments in the case of client’s default and they may not cover entity’s cost for work completed to date.

As a result, RE Construct would recognize revenue at the point of time – that is when the apartment is transferred to the client A (upon the completion in the year 2).

Revenue from contract with client B – over time

The contract with client B MEETS the third criterion.

The reason is that RE Construct cannot direct the constructed asset for the alternative use, because the contract with client B does not permit transfer of the apartment to another client.

Also, RE Construct has enforceable right to payment for performance completed to date.

Therefore in this case, RE Construct recognizes revenue over time – that is, over 2 years of construction of apartment based on some output or input method.

Let’s not go into any details of output or input methods right now. To make it simple, let’s say that 1 year prior completion, RE Construct incurred 45% of total cost for building an apartment and another 55% is incurred in the second year of construction.

As a result, RE Construct recognizes the revenue:

- In the year 1: CU 45 000 (45% of CU 100 000)

- In the year 2: CU 55 000 (55% of CU 100 000)

This example illustrates how the change in the contractual terms can drastically affect the company’s revenues.

The comparison of the revenue profiles for contract A and contract B under IFRS 15 is in the following table:

| When | Revenue for Contract A | Revenue for Contract B |

| Year 1 | 0 | 45 000 |

| Year 2 | 100 000 | 55 000 |

| Total | 100 000 | 100 000 |

Why does it matter?

Timing of revenues matters due to your tax payments, dividends, financial rations, etc. Also note, that under IAS 11, you would probably account for both contracts in the same way (as for contract B), but NOT under IFRS 15.

Maybe you should revise your contracts now and see whether you need to make some changes in order to prevent this situation.

#4 Technology and Software development

The main challenges are therefore:

- Identification of the individual performance obligations (e.g. sale of license + customization + post-delivery support) and allocating transaction price to them

- Assessment of the progress towards meeting the contract

- Assessment of the licenses for the products sold by software vendors or developers.

IFRS 15 recognizes 2 types of licenses: license to use and license to access. The accounting treatment is different for both of them and you should be able to identify which license is in question.

Other difficulties arise in areas common for every industry: dealing with contract modifications, how to account for contract costs (e.g. commissions for getting the client), etc.

Let’s take a look at example in which software company needs to split the contract and treat performance obligations separately.

Example: Software development and Splitting the contract into 2 separate obligations

ManyBits is a software company who entered into contract with a client C on 1 July 20X1. Under the contract, ManyBits is obliged to:

- Provide professional services consisting of implementation, customization and testing of software. Client C has bought software license from the third party.

- Provide post-implementation support for 1 after the customized software is delivered.

Total contract price is CU 55 000.

ManyBits assessed its total cost for fulfilling the contract as follows:

- Cost of developers and consultants for implementing and testing the existing software: CU 43 000;

- Cost of consultants for post-delivery support: CU 2 000;

- Total estimated cost of fulfilling the contract: CU 45 000.

As of 31 December 20X1, ManyBits incurred the following costs of fulfilling the contract:

- Cost of developers and consultants for development, implementation and testing the customized modules: CU 13 000.

How should ManyBits recognize revenue from this contract under IAS 18 and IFRS 15?

Revenue under previous rules (IAS 18)

Here, ManyBits clearly provides professional services and the related revenue falls under the scope of IAS 18. IAS 18 requires recognizing revenue from similar services using the stage of completion including post-delivery services.

It means that ManyBits treats software development and post-delivery services as one big service for the purpose of accounting the revenue.

Let’s say that ManyBits calculates the stage of completion based on costs incurred for fulfilling the contract.

At the end of 20X1, total incurred cost was CU 13 000, which is 29% of total estimated cost of CU 45 000.

Therefore, under IAS 18, ManyBits’ revenue from this particular contract in the year 20X1 is 29% (stage of completion) x CU 55 000 (total contract price) = CU 15 950. Sure, I used some rounding, but you get the picture.

Is it the same under IFRS 15?

Revenue under the new rules (IFRS 15)

IFRS 15 states very precise and detailed guidance on whether the goods or services promised under the contract are distinct and whether they can be considered separate performance obligations or not.

Of course, you need to perform your analysis and I tell you – your conclusion might be pretty different from this example, based on specifics in the contract.

But here, let’s say that software customization services and post-delivery support meet the definition of distinct performance obligations and as a result, they need to be treated separately.

How?

We need to look at them as at separate components, and allocate total transaction price of CU 55 000 to them based on their relative stand-alone selling prices.

Note: contract price is not necessarily the same as transaction price, but let’s not complicate it now.

Let’s say that ManyBits’ normal charge for the support services is 10% of the package price, no matter what the “package” is – whether some ready-made license or customized software.

That would imply that the relative split between customization service and post-delivery service is 100:10, which is:

- CU 50 000 (CU 55 000/(100+10)*100) for software development or customization service, and

- CU 5 000 (CU 5 000/(100+10)*10) for post-delivery support.

Again, this is just an example and some different approach might fit your own situation better.

In the year 20X1, ManyBits measures the progress towards the completion of the performance obligation separately, based on inputs for the fulfilling the contract (costs in this case).

Internal cost estimations show that ManyBits estimated total cost for the contract of CU 45 000, thereof CU 43 000 for the salaries of software developers and CU 2 000 for the salaries of consultants providing post-delivery support (based on man-days).

Let’s measure the progress towards the completion of both individual performance obligations as of 31 December 20X1:

- Software development services: CU 13 000 (incurred cost)/CU 43 000 (total estimated cost) = 30%

- Post-delivery services: CU 0 (incurred cost)/CU 2 000 (total estimated cost) = 0%

As a result, revenue recognized from this contract in the year 20X1 is:

- Software development services: 30% (progress %) * CU 50 000 (revenue allocated to software development) = CU 15 000;

- Post-delivery services: 0% (progress %) * CU 5 000 (revenue allocated to post-delivery service) = CU 0.

Total revenue from the same contract under IFRS 15: CU 15 000.

For the simplicity, you can revise the calculations in the following table:

| Performance obligation | Estimated total cost (A) | Incurred cost to 31-Dec-X1 (B) | Progress % (C)=(B)/(A) | Allocated transaction price (D) | Revenue recognized in 20X1 (D)*(C) |

| Professional services | 43 000 | 13 000 | 30% | 50 000 | 15 000 |

| Post-delivery support | 2 000 | 0 | 0% | 5 000 | 0 |

| Total | 45 000 | 13 000 | n/a | 55 000 | 15 000 |

Again, this is just one way of how new IFRS 15 can influence software developers, but also other companies performing long-term contracts.

Also, the specific calculation will strongly depend on what you have in your own contracts and how your own calculations, systems and estimates work. There is no one solution applicable for all.

Final Warning

No, there’s no mistake – I wrote WARNING intentionally.

As you can see from the above examples, new IFRS 15 can mess up with many things in your organization.

But – it’s up to YOU to analyze, make a plan and implement carefully.

My goal here was NOT to give you the full solution, because it is simply impossible without knowing your specific information.

Instead, I wanted you to be aware that you might need in fact much more time for making all the preparatory work and implementing IFRS 15 than you imagined.

I can tell you – this strongly reminds me similar situation a couple of years ago when companies needed to implement IFRS. Everybody seemed to have time when it was about 1-2 years to go before the initial date.

But when they finally started, it was painful. Then many accountants and CFOs realized that they would need much more time for making transition and they should have started months before they actually did.

Don’t make the same mistake and start NOW.

Please share this article with your friends and make them aware of what’s coming. Thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

100 Comments

Leave a Reply

Hi Silvia,

Do you have any article. How IFRS 15 had impacted Oil and gas businesses.

Thanks

Mohsi

Dear Silvia, am wondering if my company is project-based and using input-method in recognizing revenues, what is the correct approach to recognize sales discount? I am confused in if my company uses cost-plus (input) method in recognizing revenue, will I have to re-assess the “cost” as in considering the sales discount amount as part of the cost, or I just recognize the sales discount as a contra-account booking against the revenue figure?

Dear Silvia, is it possible to account penalty from contract for delay of work submitting by IFRS 15 against revenue account, i.e. reducing of contract revenues?

Dear Maria, yes, penalty is a variable consideration, so make sure you adjust the total transaction price and then the allocation to the remaining POs and revenue recognition.

Hi Sylvia

Social security organisations receive contributions pay benefits from those contributions and invest excess contributions. Two main tymes of revenue arises from these institutions:

The contributions received, Financing income and perhapsa third rental income from owned properties.

My assessment is that the aforementioned are outof scope under IFRS 15 . What are your views?

I like your write ups. They help me develop my response to challenges my students face.keep it up!

Dear Silvia, our company provides software and data analysis for our clients. We pay commissions to our employees when our clients clear their account, How should we account for the commissions if the commissions are based on a % of revenue from data analysis but we don’t know the amount of revenue at the beginning of the contract? We prepare invoices once per month, based on the number of data analysis dispatched every month, and then once the client pays, we calculate the commissions for the employees.

Hi silvia,

Just want to clarify followings.

1.How should a company account for Gift Voucher revenue?

2.Do we need to classify expired gift voucher revenue under other income? Hence the Cost Of sales is not charged for the expired gift vouchers?

Hi Hirantha,

1) Well, you do not recognize revenue until you satisfy a performance obligation (whatever that is). E.g. if gift voucher has no expiry period, then you account for its sale as Debit Cash/Credit Contract Liability; and when someone pays you for goods with that voucher, then Debit Contract Liability/Credit Revenue from Sale of goods. If that voucher has an expiry period, and when no one comes to pay with the voucher, then you might book revenues as Debit Contract liability/Credit Revenue from expired vouchers.

2) You may if this is material. S.

Hi Silvia you are making IFRS easy, Thank you very much indeed. I always read your articles. I am benefiting byclearing my doubts and confusions. Please Keep it up.

Hi Silvia,

Is this correct?

Revenue could not be recognized until both parties had signed the terms and conditions of the contract. However, under the latest FASB/IASB proposed model, the signed contract rule is no longer applicable.

Hi Silvia,

Thanks for the examples above. I am not sure I follow the second scenario under the manufacturing contract modification case.

You have mentioned in your example “We need to allocate CU 680 000 to 400 computers in total (200 undelivered before contract modification + 200 additional computers), which means that Ball PC allocates CU 1 700 to one computer (680 000/400).”

I understand from your example that the additional computers under the contract modification are distinct, still you have allocated the total price to the computers not yet delivered under the original contract AND the computers under new contracts. So, basically allocating total price to two different types of products.

Could you please clarify the above?

Many thanks!

Dear Silvia,

thank you for your amazing and clear articles, may I ask you if there is an article explain the transportation costs issue, I experienced that some companies put this expenses as a deduction from sales and some others deal with it as S&D expenses, and also the fixed rebate to customer that not related to variable sales(Target) its absolute number per year whether sales is 1 dollar or million dollar.

thanks,

Hi Silvia, thank you for the great sharing, When I first read the standards/guides, it really causing me headache, I have no clue what is it talking. Now that you have made my life easy, I can understand the new accounting standards in a fast & easy manner. Fall in love with your materials.

May I find out from you for an advertising published in a quarterly issued magazine, do we consider that under point in time or over the time? Say if the advertisement is published in a magazine that labelled as Apr-June 19 edition. I would think the performance obligation is done when the advertisement in the magazine is distributed in the market, but the consumption of the advertiser will be across Apr to June 2019. Appreciate your advice.

Hi Heather, thank you! Well, in my opinion it is at the point of time, since you need to assume the delivery of a service, not its consumption pattern. In this case, you deliver service at one point by publishing a magazine. S.

Hi Silvia,

I have questions regarding incoterm CIF. When should revenue be recognised when:

1. The insured is the buyer

2. The insured is the seller

3. Transhipment where goods will be shipped to the buyer’s customer.

Should revenue be recognised when the goods passes the ship’s rail or upon reaching the buyers port?

Thank you

Kelvin

Hi SIlvia,

I have a question regarding recognising revenue for online or website sales for consumer goods. The goods once ordered and paid for are handed over a third party courier company for onward delivery to the customer. Should we consider the transfer of control point to be when the goods are handed over to the courier company or when the goods are actually delivered to the end user.

THanks

Hi Silvia

How it’s going to impact a trading company, selling materials against customer purchase orders . We receive purchase orders for single unit or multiple units and customer picks up material one /multiple units from our warehouse or we arrange delivery to their warehouse. Payments against this delivery will be on agreed payment terms.

Hi Sreekumar, if it is that simple, then I would say the treatment does not change. The only thing is that you should really trace multiple deliveries of one order – in this case, you should recognize revenue partially when each delivery is made. S.