How The Groups Change

Group accounts are a very popular topic and yes, I can understand it as it’s a main topic for many accounting exams.

I have written a few articles about it, including:

and a few summaries of standards dealing with these issues, such as IAS 28, IFRS 3, IFRS 10 and IFRS 11.

Today, I’d like to go beyond basics and clarify what happens when a group changes its composition.

In other words – what happens when an investor decides to acquire more shares or as opposite, dispose of some shares in its existing investment.

It’s very hard to name and count all the ways of changing group’s composition. Here, I tried to outline just a few of them -let’s call them “basic”.

Having that said, there’s a number of tweaks and twists and you need to consider and evaluate each situation very carefully to select the most appropriate accounting treatment.

The ONE THING to remember

When an investor purchases new shares or sells some share in the same investee, then the principal question is:

How does the relationship between an acquirer (e.g. parent) and an acquiree (e.g. subsidiary) change?

In other words, what is the relationship before change and what will it be afterwards?

Let me explain.

There are 4 different types of relationships between investors and investees:

- Control, as defined by IFRS 10;

- Significant influence, as defined by IAS 28

- Joint control as defined by IFRS 11

- None of the above – in this case, an interest in an investee is considered a financial instrument under IAS 39/IFRS 9.

For the simplicity, let’s not deal with joint control here, but in most cases, when joint control is involved in the change, the accounting treatment is the same as for significant influence.

Also, in this article, I focus on groups with control only – either when control is acquired, maintained or lost. In the future, I will write up something specifically for significant influence, too.

Let’s explain what we should do when an investor purchases more shares, or sells some shares in the same investment.

Purchasing more shares

When an investor acquires more shares in its investee, then there are a few ways how control may change:

- No relation increases to control (e.g. 15% share is increased to 70% share);

- Significant influence increases to control (e.g. 25% share is increased to 70% share); or

- Existing control is maintained while new shares are acquired (e.g. 55% share is increased to 70% share).

Let me remind you that the share amount is just an indicator and in practice, control can be achieved in a different way, for example contractually without changing the shares.

Let’s take a look at the accounting treatment.

No relation -> control

When an investor acquires control in its investment with no significant influence, then in fact, a subsidiary is acquired and you need to consolidate.

The principal questions are:

- What to do with a previous investment?

- How to calculate goodwill?

#1 What to do with a previous investment?

You simply dispose it off and derecognize it from the financial statements.

I know, I know – the rules for derecognition of financial instrument are not met here. But, this is only a “deemed disposal” and you will re-recognize the same investment together with new shares.

You need to calculate investor’s gain (or loss) from deemed disposal (fair value less carrying amount) and recognize it in profit or loss.

Then, right after you do it, you recognize your previous investment back at fair value, together with your new investment.

#2 How to calculate goodwill?

As you know by now, goodwill is calculated as:

- Fair value of consideration transferred, plus

- Non-controlling interest in an acquiree, plus

- Fair value of previously held interest when acquisition happens in stages , less

- Net assets in an acquiree.

Therefore, you simply include the fair value of previously held interest in the calculation of goodwill and then you consolidate as usual.

But, to make it clear, let’s illustrate it on a simple example.

Example: No relation -> control

ABC holds 10% share in DEF and it acquires another 50% in DEF on 30 June 20X1. At this date, control is achieved. The financials on 30 June 20X1 are as follows:

- Carrying amount of 10% share in ABC’s books: CU 1 000

- Fair value of 10% share: CU 1 300

- Cost of 50% share that ABC actually paid: CU 6 700

- DEF’s net assets: CU 11 000

First, let’s calculate gain on a deemed disposal:

-

Debit Financial investments: CU 300

-

Credit P/L – Gain on a deemed disposal: CU 300

Then, we can calculate goodwill:

- Fair value of consideration paid for 50% share: CU 6 700

- Fair value of previously held interest: CU 1 300

- Non-controlling interest (CU 11 000*40%): CU 4 400

- Less DEF’s net assets: CU 11 000

- Goodwill: CU 1 400

Then you can go ahead and consolidate – here’s my article with a basic consolidation example.

Significant influence -> control

When an investor acquires control in its associate (with significant influence), then an associate ceases to exist and subsidiary is acquired.

The accounting treatment is exactly the same as shown above. You need to:

- Derecognize an associate and calculate investor’s gain on a deemed disposal; and

- Recognize a subsidiary and start consolidating.

Both steps are identical as above. Derecognition of an associate is not a big issue as an associate is shown as a single line item exactly as a financial investment above.

Control is retained with more shares acquired

When an investor has already controlled an investment before acquiring an additional share, then an accounting treatment is totally different from previous two situations.

Why?

Because, an investor does NOT acquire a subsidiary with an additional purchase.

As a result, you should NOT derecognize previously held investment with profit or loss on a deemed disposal.

What happens here instead is that an investor buys a greater percentage of ownership of subsidiary’s net assets.

Therefore, you need to adjust parent’s equity to show there was a transfer between owners.

How?

By purchasing additional share, a non-controlling interest decreases because it is sold to a parent.

Also, there might be some transfer between non-controlling interest and retained earnings to reflect the changes in fair value over time (at the date of additional acquisition versus date of the first acquisition).

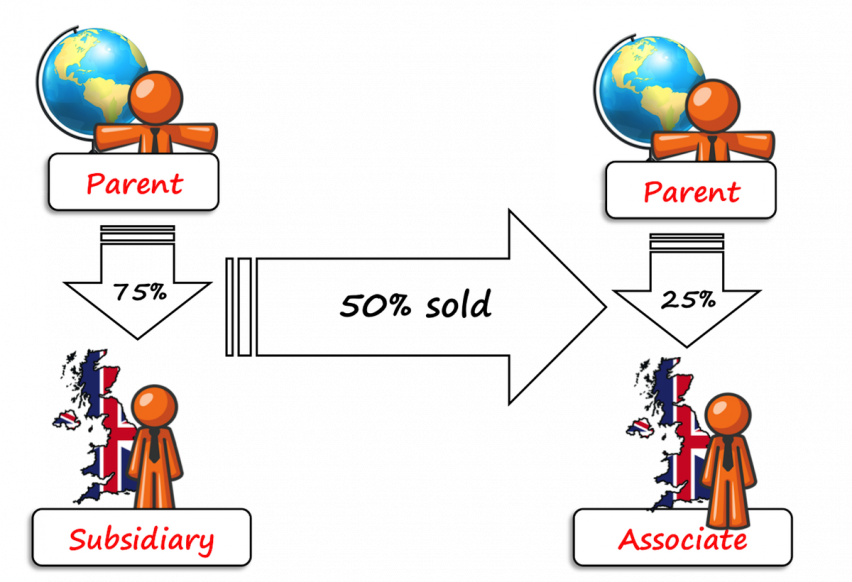

Disposing of some (or all of) shares

When an investor sells shares in its subsidiary over which control is exercised, then there are a few ways how control may change:

- Control is lost and significant influence is acquired (e.g. 70% share is decreased to 25% share);

- Control is lost and no significant influence is acquired (e.g. 70% share is decreased to 15% share); or

- Existing control is maintained while some shares are sold (e.g. 70% share is decreased to 55% share).

Be careful here, because in reality, an investor does not need to sell anything to dispose of her subsidiary. In other words, a subsidiary can be disposed of by other ways, for example:

- Another investor exercises its options to get shares in a subsidiary (as a result, parent’s share is reduced);

- A subsidiary issues shares to third parties,

- A new contract transfers control from a parent to someone else.

In these situations, control is lost and subsidiary is disposed of. This is called “a deemed disposal” and you must be extremely watchful what’s happening around you, because sometimes a subsidiary can be disposed of without a parent even noticing (OK, that would be an extreme case, but still possible).

In principle, the accounting for these situations is very similar as written above, just the other way round. What really matters here is whether control is lost or retained.

Let me sum it up.

Control is lost

When control is lost, then an investor (or a parent) disposes of its subsidiary and stops applying the full consolidation method.

Be careful about the situations when the parent sells shares, but keeps control – in this case, a subsidiary becomes a special purpose entity and you still need to consolidate.

If you truly dispose of subsidiary, you need to take 2 steps:

- The first step is to calculate gain or loss from disposal of investment, in both parent’s separate financial statements and consolidated financial statements (yes, these 2 numbers are different).

- The second step depends on what share or interest in an investment is retained:

- If all investment is disposed of, then there’s no second step 🙂

- If an associate is acquired (e.g. 70% share decreases to 25% share), then the remaining investment is recognized at fair value at the date of disposal, and from that date, an equity method is applied;

- If an investment with no significant influence is retained (e.g. 70% share decreases to 15% share), then an investor must classify the financial asset and continue measuring and recognizing it in line with IFRS 9.

Control is retained

When an investor decreases its share, but retains control (e.g. 70% share decreases to 55% share), the situation is pretty different.

You need to continue consolidating, because you still have a subsidiary.

Also, despite disposing of some shares, you do NOT calculate any gain from disposal.

Instead, this is accounted for as an equity transaction – that is, as a transaction between the owners of a subsidiary. More precisely, you should adjust only a non-controlling interest and retained earnings within equity. Assets and liabilities remain untouched.

How do we present comparative information?

To finish this article, I’d like to make a note about comparatives.

Very often I get one and the same question:

“We acquired/sold a subsidiary during 20X2, should we restate the comparative numbers for 20X1, too?”

The answer is NO.

The reason is that here, you did not change any accounting policy that would require a restatement.

Instead, acquiring or selling a subsidiary is a new event occurring in the current reporting period, but not in the past. Therefore, it’s totally OK to present comparatives as they are. You are only reflecting a fact that your group looked differently in the comparative reporting period.

In this article, I tried to outline the basic ideas around the changes in the groups, without aiming at providing an exhaustive and complete explanation – that would take me a book! Please feel free to share this article with your friends who can benefit. Thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

30 Comments

Leave a Reply

Considering the group structure consists of ultimate holding company A, parent company B and subsidiary C.

In past years, the parent company B had not been preparing consolidated accounts for subsidiary C as the ultimate holding company A had been doing so. In current year, ultimate holding company A sold off it’s shares in the parent company B. Question: Does the parent company B need to present consolidated accounts for prior years since it is require to prepare consolidated accounts this year.

Hi Silvia, many thanks for your article on this subject. I have a scenario where there is increase in parent’s ownership in subsidiary from 60% to 90%, where parent subscribed for entire additional shares issued by the subsidiary.

Here, in the consolidated financials, since no consideration is paid for additional acquisition, there will only be a transfer of previous 40% NCI value to Parent’s equity?

Thanks

Kay

Hi Silvia, great explanation just wanted to inquire one detail, if we take the above example in regards to What to do with a previous investment – where I recognize previous investment back at fair value, together with new investment. This will be the amount presented in Separate Financial Statement ? and will I be able to account for it as cost (in accordance with ias 27)

Thanks in advance

Hi Silvia- I want to study above in more detail. Kindly suggest if IFRS Kit covers the Excel based examples to cover Group accounts consolidation and consolidation in details. I will be happy to learn more through IFRS Kit.

Thanks

C

Hi Silvia,

Kindly help in following scenario.

Company A is owned by 3 parities as follows:

1) Company B 46%

2) Company C 46%

3) Company D 8%

Now company C decided to sell its 46% share to company B with agreed amount of XYZ which results in 92% ownership of B in A.

Company B initially recognises its ownership as Long term investment in A.

Can you kindly guide which method is applicable in this case and what would be journal entries in Company B books for additional purchase of 46% shares ?

Thanks

Hassan

Hi Sylvia,

Which consolidation method to use when the parent company does not have any activities.?

Thank you!

Julie

Hi silvia ,

if i have an investment in association turn to a subsidiary, when preparing consolidate financial statement how to present comparative figures in consolidate financial statement

Hi d,

you do not restate anything, because in the previous reporting period, there was no subsidiary. So you present this investment as an associate in comparatives and as a subsidiary (full consolidation) in the current reporting period. S.

Hi, my question is how to deconsolidate a indirect subsidiary? Parent had direct interest of 18% of C, and control B is 55.3%, and B control C is 52%, parent has 46.76% indirect interest in C. How to deconsolidate C company?

Sorry Silvia,

I think the entries should be:

Dr. investment in Subsidiary 6600

Dr. Goodwill 1400

Cr. Cash 6700

Cr. Financial investment 1300

Thanks

Alice

Hi Silvia,

For your illustration 1 above No interest to Control: the updated BS would be:

Investment in Subsidiary 8000 (1300 + 6700)

Goodwill 1400

Financial investment 0

NCI (4400)

are these correct?

Also what will be the journal entry for the goodwill? Dr. Goodwill / Cr. ??

Sorry if the question is too naive.

Many thanks

Alice

Dear Sylvia,

I am a tutor at Kokopo Business College Papua New Guinea, teaching Financial Accounting for second year Diploma in Accounting. I would like to purchase the IFRS kit not with the internet payment but manually at the Western union.

In the meantime will you be able to help me if I sent you a topic of notes I will be covering with the latest notes or developments if accounting standards.

My first topic will be on Accounting for Group Companies- Consolidated Financial Statement and its relevance to my country in the South Pacific, Papua New Guinea.

Thank you

Dear Aiva,

thanks a lot for writing me! If you want to get the IFRS Kit, you can pay us either online or via SWIFT/direct wire transfer – we do not accept western union payments. For the notes, please sign up for my newsletter. S.

Dear Silvia,

My company has two subsidiaries with holding of 65% and 100%. The subsidiary with our 100% shareholding was acquired by our subsidiary with 65% shareholding at a swap ratio of 100:96.43. How do we show the investments in our books:

We were planning to pass the following entry:

Investment in share of subsidiary with 65% shareholding ……..Debit

Loss on disposal of share of subsidiary with 100% shareholding …………..Debit

Investment in share of subsidiary with 100% shareholding ……………………..Credit

Or, should we just pass the following entry without booking the loss and show the investment at Rs.104

Investment in share of subsidiary with 65% shareholding ……..Debit

Investment in share of subsidiary with 100% shareholding ……………………..Credit

Please advise.

Thank you

Nalini

Hi Nalini,

I would go for the first alternative, because you always need to recognize the new acquisition at fair value and that could be different from the carrying amount of derecognized asset. S.

Dear Silvia,

My company has 1 subsidiary and prepares consolidated financial statements in FY2015.

If the company disposed of the subsidiary during FY2016, how would the 4 statements namely the balance sheet, statement of profit or loss and other comprehensive income, statement of changes in equity and statement of cash flows look like? Is the following presentation correct?

(1) Balance sheets for the Group and the Company for FY2016 and FY2015, (or just FY2015 for the Group, as there is no subsidiary at the end of the year?).

(2) Statement of profit or loss and changes in equity for the Group and the Company for both FY2016 and FY2015.

(3) Statement of cash flows of the Group for FY2016 and FY2015? How about the Company?

(4) or, can the company remove completely the Group figures for FY2015 and present the company figures only for FY2016 and FY2015, with disclosure notes saying the subsidiary was disposed of during FY2016?

Thank you and have a nice day.

Kelvin

Dear Silvia,

Good day.!

Hi, I am CMA student preparing for Professional Level, question which I asked related to disposal of subsidiary covered in CMA Financial reporting book.

I refer your article, but I am still confused with the entry to be posted in Group Books. I understood that at 100% disposal of subsidiary profit or loss will be different in both books (At Parent Co. Book and At Group) but what will be the entry posted in Consolidation books of account. In following scenario;

In the books of subsidiary (which is disposed by group):

Net Fair/carrying Value of Assets :1000 USD as at 31.12.2013 (SC= 400 comprises of 200 Shares having face value of 2 each share), Retained Earnings=600)

Net Fair/carrying Value of Assets :1200 USD as at 30.04.2014 (SC= 400, Retained Earnings=800)

Cost of investment in parent books as at 31.12.2013: 400 USD

Retained Earnings in Consolidated books of account as at 31.12.2013: 1800 (Parent books profit 1000+ Subsidiary Profit =600) (no intercompany transactions)

On 30.04.2014 parent company sold 200 shares of subsidiary at 6 USD per share i.e. 1200 USD, and received in cash 1110 after withholding tax 90 USD (11.25% Tax bracket calculated (1200-400) =800*11.25% =90 USD) tax expense born by Parent Co.

Profit in the books of Parent Co,

Cash A/c …..Dr 1,110

Tax Expense A/c ….Dr 90

Investment in Co. A/c….Cr 400

Profit on disposal of Investment ….Cr 800

My question for consolidation is;

Whether to report USD 200 (800-600=200 incremental retained earnings for 4 months) as profit from discontinued operation or not? (as till 31.12.2013 10% share of profit already accounted in Consolidation in 31.12.2013)

What will be the accounting entries to be posted in Consolidation Books?

Thanks, in advance.

Regards/VM

Sorry, Volten, this is too complex question to be replied in the comments. I’ll write an article about that, but not in the comments. Also, this case is solved in the IFRS Kit. Thanks. S.

Hi sylvia, im thinking of buying ifrsbox but I just can’t afford it becaue 1 euro cost 59.00 in my country and I’m still a student in review for CPA board exam … would you consider giving discounted price for student? 🙂 Thanks.

Dexter, please write me via Contact form. Thanks, S.

Many thanks to you Silvia.

Hi Silvia,

Thanks for the article.

One place you mentioned that a “subsidiary can be disposed of without a parent even noticing “. This made me curios to know how it would be happen. Grateful if you can explain with a example.

Thanks and regards.

Chinthaka, right the next sentence says that it would be an extreme case. I described the situations right above that paragraph 🙂 For example, when subsidiary had some convertible instruments and some third parties decided to exercise the conversion options + got the shares – in such a case, parent’s interest can be reduced by additional shares issued and control can be lost. S.

Thank you for updating my knowledge level

thanks my teacher

Thank you very much Sylvia.

Thanks Sylvia, so grateful.

Many thanks for the article.

Thank you Sylvia

Most informative

Thanks Sylvia,for keeping me more current on Changes in a group structure..