How to Make Cash Flow Projections for Impairment Testing under IAS 36

Impairment tests are one of the most judgmental areas in IFRS.

It is all about estimating, judging, evaluating and forecasting.

Sometimes it is almost like fortune telling, isn’t it?

When I audited a few companies, I really disliked going through their impairment tests because all of them seemed nice and always showed no impairment whatsoever.

However, digging deeper into the assumptions and numbers can give different results.

Often I found too unrealistic assumptions, wrong discount rates, incorrect items included in the cash flow projections, etc.

Here, I would like to shed some light on the cash flow projections that are most judgmental, yet one of the most important elements in the impairment testing.

Why cash flow projections?

In fact, cash flow projections are crucial in the impairment testing for two reasons:

- They are the basis for determining the asset’s or cash generating unit’s (“CGU”) value in use.

When you are setting the value in use, you are estimating how much value the business gets out of the asset when using it or consuming it. - When there’s not enough market data, cash flow projections are the main input into fair value calculation.

However the difference from value in use is that in this case, you are estimating cash flows based on what the market is willing to pay for your asset or CGU under review.

What do the rules say?

The standard IAS 36 (article 33) gives the basic rules to follow when establishing your cash flow projections for the impairment testing:

- Use reasonable and supportable assumptions as a basis for your cash flow projections. They must reflect management’s estimate of economic conditions over remaining useful life of the asset while greater importance is given to external evidence.

- Use the most recent financial budgets or forecasts approved by the management, while:

- Exclude future cash flows from restructuring or improving or enhancing asset’s performance;

- Cover a maximum of 5 years, unless you can justify using longer period.

Then the standard IAS 36 guides you further in preparing your cash flow projections.

Let’s sum up the main considerations and pitfalls here.

How to set your cash flow projections?

The main ingredient in preparing your cash flow projections is common sense.

I cannot stress it well enough – just use your good, down-to-earth judgment.

Just as an example, imagine you set up a successful start-up and developed a simple gadget with revolutionary technology and features.

Your sales have been increasing at the rate of 200% each year for the past 3 years.

You are performing impairment testing of your CGU and in your cash flows you incorporate the growth rate of 200% for the next 5 years.

You have achieved this rate in the past 3 years, then why not in the future?

Well, if you find out that at the end of year 5 you plan to sell 10 billions of these super computers based on that growth rate, while total population on earth is just 7 billions – then there’s a problem, isn’t it?

Definitely, common sense lacks.

This was a bit unrealistic illustration, but I think it did its job!

Always bear in mind that your cash flows must be reasonable and supportable.

Here are a few tips to make it happen:

- Use approved budgets and forecasts.

- Put great importance on external information. Look out for industry reports, experts’ valuations, forecasts about economy, etc. Try to be consistent with this information as much as possible.

- Always check your forecasts to market data. Did you incorporate growth rate despite the fact that there’s deflation forecasted for your area? Well, then you need to justify it.

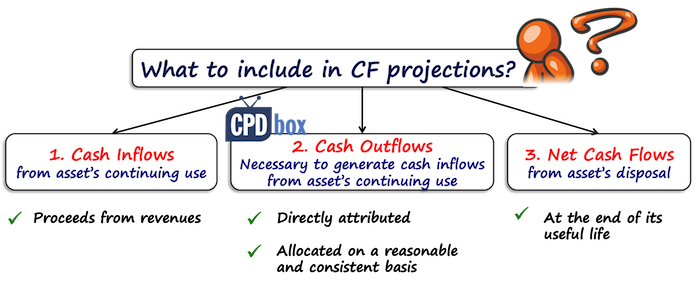

What to include in and what to exclude from your cash flow projections?

The standard IAS 36.39 sets three basic elements to include in your cash flow projections:

- Cash inflows from the continuing use of the asset.

These mainly include proceeds from revenues generated by the asset or CGU. - Cash outflows necessarily incurred to generate cash inflows from continuing use of asset which are directly attributed or allocated to the asset on a reasonable and consistent basis.

Here you would estimate day-to-day servicing costs, maintenance costs, general and production overheads and similar items. - Net cash flows from the disposal of the asset at the end of its useful life.

There are a few difficulties that arise when deciding whether to include or exclude certain item in your cash flows projections.

Let me tackle them shortly:

1. Maintenance vs. improvement

While you need to include maintenance costs into the cash flow projections, you should strongly keep in mind that these cash flows only include items for assets or CGUs in their current condition.

Thus, you should NOT include neither any outflows to be incurred for improving or enhancing the asset’s performance, nor any inflows resulting from enhanced asset.

Do NOT recognize improving capital expenditure, but DO recognize replacement and servicing expenditure to maintain the asset’s capacity.

However, sometimes it is quite difficult and challenging to distinguish between maintenance and improvement expenses and some judgment is always needed.

There are two exceptions permitting you recognize enhancing capital expenditure in the cash flow projections:

- Asset in progress – If you have already invested into generating of some asset, but it has not been finished, then you should include all expected cash outflows required to make that asset ready for use or sale (see IAS 36.42).

- Restructuring – If your company becomes committed to restructuring in accordance with IAS 37, then you can include the results of that restructuring into cash flow projections. Just be careful here, because you need to meet certain conditions set by IAS 37 in order to conclude that you are committed to restructuring.

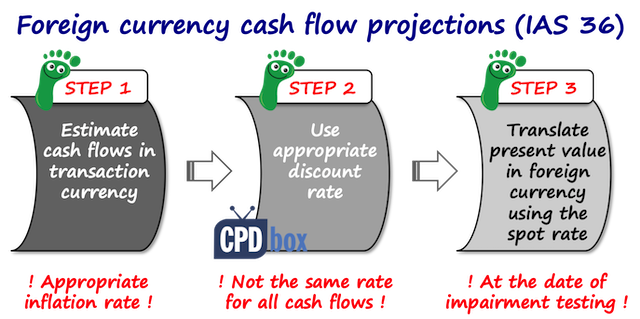

2. Foreign currency cash flows

If you incur foreign currency cash flows related to asset or CGU under testing, then you have a big complication here.

In fact this is quite common – some company may produce its products in a country with a functional currency of EUR and most of cash outflows will be in EUR.

The same company may sell all of its products solely to three clients in three different currencies: USD, GBP and EUR.

How to include forecasted cash inflows in USD and GBP into the cash flow projections in EUR?

Let me list a few steps:

- Estimate cash inflows in the transaction currency and do not translate forecasted revenues in the functional currency.

In our small illustration, all revenues in USD will be included as cash inflows in USD; the same applies for GBP.Here, I’d like to warn you about the inflation rates. When you are estimating cash flows in foreign currency, be careful about incorporating the growth rate and inflation rate appropriate for that currency.

I have seen already that some companies forgot about that and applied the same growth rate to all cash flows irrespective of the currency.

- Use the appropriate discount rate. You need to realize that the economic environment in the USA is different from that in Eurozone and as a result, the interest rates and discount rates are different.

- Translate present value of foreign currency cash flows to the functional currency using the spot rate at the date of impairment testing.

This method is prescribed directly in IAS 36.54.

You should NOT use any forward exchange rates, because you would be double counting.

Why?

Well, forward exchange rates are determined based on the differences between the interest rates of the countries with these currencies.

And, you have already included different interest rates in your calculations by using different discount rate for the specific currency.

3. Intercompany charges

Another frequent situation is when your company makes intragroup sales or purchases and needs to include cash flows from these transactions into its projections.

You should always include these transactions at estimated market values, with some adjustments for discounts or other items (as soon as it reflects the “arm’s length”).

4. Receivables and payables

In general, you should NOT include future cash flows related to settlement of receivables, payables and tax liabilities into the projections.

The reason is to avoid double counting.

However, if it is more practical for you, then you can include settlement of these balances into the cash flows, but in this case you need to be consistent and include the amount of receivables, payables and tax liabilities into the carrying amount of your CGU under testing.

If you have a liability that has to be considered when determining recoverable amount of CGU, then you must include the cash outflows related to that liability to cash flow projections.

For example, imagine you are testing a nuclear power plant for the impairment.

You have to include the decommissioning liability cash outflows into account since this liability is attached to the nuclear power plant.

Oh, and what about the repayment of loans?

In general no, you do not include these if you excluded loan liability from CGU being tested.

You also need to ignore interest payments, because cost of your capital is taken care of by discounting.

5. Terminal value

If you are testing an asset with an indefinite life, or with a useful life beyond forecasted period, then you need to include terminal value in the cash flow projections.

It is quite common that the terminal value represents more than 50%, sometimes even 80% of the total present value of your cash flow projections, therefore it is absolutely crucial to get it as right as possible.

In many cases, the terminal value is just the net proceeds that you expect to get from the sale of an asset at the end of its useful life – especially when that end happens to be the end of your cash flow forecasts.

In other cases, the terminal value is the estimate of what you would get for the cash flows beyond your forecast period.

Imagine you run an indefinite business, you don’t know when it will terminate generating cash flows and you are able to make reliable forecasts for the next 5 years.

How to cover the period beyond 5 years?

For how much would you sell that business after 5 years?

Two most common methods to calculate it are:

- Exit multiple – this is the multiple of shareholders’ cash flows in the last year of projections.

- Perpetuity – you would take the last year’s projection and apply perpetuity formula to it. The result would be indefinite projection of cash flow in one number.

In fact you are calculating growing perpetuity as a series of periodic payments that grow at a proportionate rate for an infinite amount of time.

There could be great differences in the terminal value when calculated either way and the reason is that as you are giving up on business risk when selling a business, your terminal value can be lower when applying exit multiple.

Thus use the method consistent with the management’s estimate of the company’s destiny at the time of performing the impairment testing.

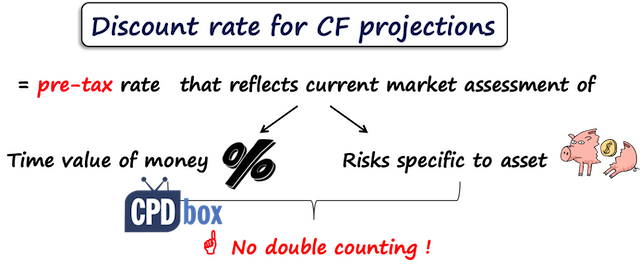

6. Discount rates for the impairment testing

The discount rate used to bring the cash flow projections to their present value should be:

- a pre-tax rate

- reflecting the current market assessments of the time value of money; and

- incorporating the asset-specific risks for which the future cash flow estimates have not been adjusted.

Practically, you can use:

- Market interest rate that is incorporated in the current market transactions for similar assets, or

- Weighted average cost of capital (WACC) of a listed entity having a single asset or a portfolio with similar service potential and risks to the asset under review, or

- Surrogates, such as:

- Your own WACC;

- Your own incremental borrowing rate; or

- Other market borrowing rates.

Having that said, you need to be careful enough to incorporate all the necessary risks that were not incorporated into your cash flows and vice versa.

You cannot incorporate the same risk to both discount rates and cash flows, otherwise it would be double counting.

You need to use pre-tax rate, while sometimes the rates are set post-tax. In this case, here’s the article on how to calculate pre-tax rate from post-tax rate.

Finally, remember that some cash flows might require using different discount rate.

For example, when you have cash flows denominated in a foreign currency, or cash flows with different risks.

It would be appropriate to use WACC for low-risk assets like buildings, but if you test riskier assets like brands, or start-ups, then you might need to adjust discount rate for higher risk.

How many scenarios?

When I audited impairment tests in some companies, they presented only one single cash flow projection.

Well, if you are an auditor, you should be aware of human psychology, too.

Sometimes, business people tend to be over-optimistic and thus management often includes too optimistic views of their future performance into cash flow projections.

Unless the management is a great prophet who proved to forecast the numbers with 90% reliability in the past, this approach is a bit risky and not really substantive.

Did you look to your forecasts 3 years ago and compare them to the present results? How precise were you?

Of course, no one wants management to be a fortune-teller and having a crystal ball standing on their desk, but if the management was not so precise in their forecasts, maybe it is time to include more than one scenario of cash flow projections.

You may prepare one cash flow projection for the great times, one for the miserable times and one if the things go as expected.

Then you need to weight these cash flows by probabilities of happening and calculate expected cash flows.

Alternatively, you can use the traditional approach and incorporate the risks and uncertainties to your discount rate – which I find more difficult.

Final word

I planned to include the numerical example in this article, but when I thought about it, I decided not to.

The reason is that there are so many calculations and illustrations to show you and thus I decided to do the separate article with the example illustrating the calculations.

Update: Here’s the article with numerical example illustrating the above mentioned concepts. Enjoy and please share!

Stay tuned and please leave a comment below if you wish. Thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

14 Comments

Leave a Reply

Hi,

Would like to clarify on the exclusion of loan repayment from the Cash Flow projection. How is the idea if we were to include the loan liability for the CGU being tested?

Thank you Silvia. For a company that is engaged in the business of payday loans which are being financed from borrowings from banks, can we include such borrowings in our cash flows while calculating a ‘value in use’? Thanks

Thank you for your informative lesson

Great article and I think the most challenging part is to identify the correct “CGU” sometime. There are so many areas covered under this impairment modules such as PPE, goodwill, investment in subsidiaries, associates and joint arrangement and intangible assets etc.

I look forward to your illustrative example Sylvia and thanks for your great work!

Keep it up my hero. This is a great contribution for us.

Thank you

Thanks, Silvia for the article. it really helpful

Very helpful article

Thanks Silvia for your very useful explanations. IAS 36 has been my challenge but am getting the facts at the moment.

I But I wish you should have done some bit of calculation samples for better understanding in terms of figures.

I also went you to explain impairment in relation to IAS 16 in the aspect of cost model and revaluation model.

Thanks Again

Very helpful indeed.

Hi Alexander, thank you! As I wrote above, I am planning to publish an article solely with calculations to illustrate these concepts. S.

Thanks so much Silvia, I also wait for the next article of illustration

Value loaded article..Thanks Silvia

Very useful article. Thanks Silvia ?

Thank u for such an important article Silvia. I shall purchase your IFRS package soon.