Example: IAS 33 EPS and Rights Issue

Earnings per share (EPS) is one of the two ingredients for calculating PE ratio (or P/E ratio) – one of the most significant and important indicators of a performance of certain stock or share in the stock market.

As I have already written in this article, the two ingredients are:

- Market price per share – the numerator; and

- Earnings per share – the denominator.

The standard IAS 33 Earnings per Share give us the rules for calculating EPS, to improve comparability of the financial performance of different entities, or even of the same entity over time.

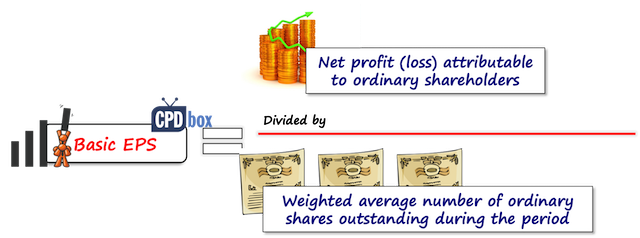

The basic formula

As its name suggests, EPS is calculated as

- The net profit or loss for the period attributable to ordinary shareholders; divided by

- Weighted average number of ordinary shares outstanding during the period.

Weighted average number of shares

While the numerator – the net profit/loss for the period attributable to ordinary shareholders – is quite easy to determine, some challenges may arise when determining the weighted average number of shares.

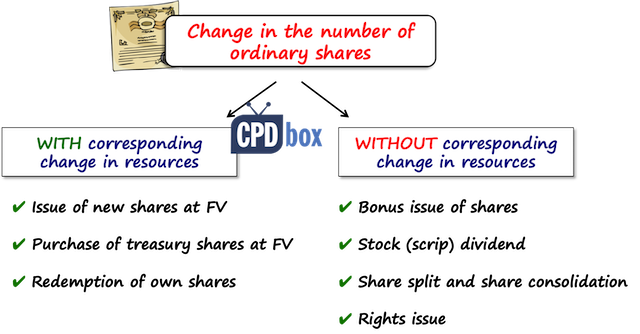

There might be various events affecting the number of shares outstanding during the year and I would classify them in two groups:

- Those with corresponding changes in resources;

- Those without corresponding changes in resources.

Let’s take a look.

Changes in ordinary shares WITH corresponding changes in resources

When there is a change in the number ordinary shares and there is a corresponding change in resources (e.g. cash), then the calculation is fairly simple and easy.

The examples of such a change are:

- Issue of new shares for cash at fair value;

- Purchase of treasury shares for cash;

- Redemption of own shares.

You can revise Example 1 of basic EPS calculation including these changes here.

Changes in ordinary shares WITHOUT corresponding changes in resources

Sometimes, there is a change in the number of ordinary shares without the change in cash or other resources.

The standard IAS 33 lists a few examples of similar changes:

- Bonus issue, capitalization – here basically the new shares are issued with zero increase in resources. Please see here for Example 2 solving basic EPS with bonus issue.

- Stock dividend or scrip dividend – similar as above. Here, the entity pays the dividends to its shareholders in form of new shares instead of cash. Again, the change happens with zero increase of resources.

- Share split, share consolidation – Either one share is split into a few shares (= share split), or the opposite happens – an entity consolidates its share capital into smaller number of shares (e.g. “merges” 2 shares into 1 share = share consolidation; also called reverse share split). There is zero increase (in the case of split) or zero decrease (in the case of share consolidation) of resources.

- A bonus element in any other issue – for example, rights issue. This change is different from previous 3 changes, because here, there is an increase in the resources, but not at fair value and it does not corresponds fully to the increase of number of shares.

Rights issue – what is the problem?

A rights issue is the situation when the existing ordinary shareholders can purchase additional ordinary shares, typically with some discount to the fair value of the shares.

Rights are usually granted pro-rata to all ordinary shareholders.

For example, a company ABC offers all its ordinary shareholders the right to purchase ONE ordinary share for every FOUR ordinary shares that they hold, at 30% discount to the fair value (market price).

So imagine you have 1 000 shares in ABC and one share trades for CU 10 at the stock exchange. With this offer, you can purchase additional 250 shares (ONE new for your FOUR existing; that is 1 000/4 = 250) at 30% discount – that is, at CU 7 per share.

Isn’t this nice? On the stock exchange, you would have to pay CU 10*250 = 2 500 for your 250 new shares, but now, with the rights issue, you pay only CU 7*250 = 1 750.

However, there is one complication in relation to EPS calculation:

From the ABC’s point of view, the increase in shares by 250 does NOT correspond to increase in resources – these increase by 1 750 only, not by 2 500.

This is a bonus element and we must take this into account in our EPS calculation.

Note – if the offer was to purchase one for four shares at the market price, there is no complication as there is no bonus element.

How to adjust number of shares for rights issue?

In fact, a rights issue is simply a bonus issue (issue of new shares with zero increase in resources) mixed with an issue at fair value.

When there is a bonus element in any issue, then IAS 33 requires retrospective adjustment to the weighted average number of shares for both basic and diluted EPS.

What adjustment?

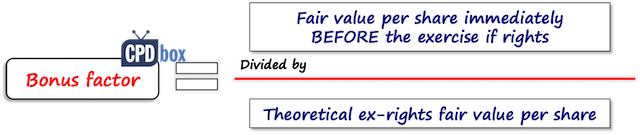

IAS 33 calls it a “bonus factor” and it is calculated using the following formula:

Let me explain the two parameters of this formula:

- Fair value per share immediately before the exercise of rights = this is typically the market price per share immediately before it becomes “ex-rights” – or, at the last day when the shares are traded together with the rights (“cum-rights”).

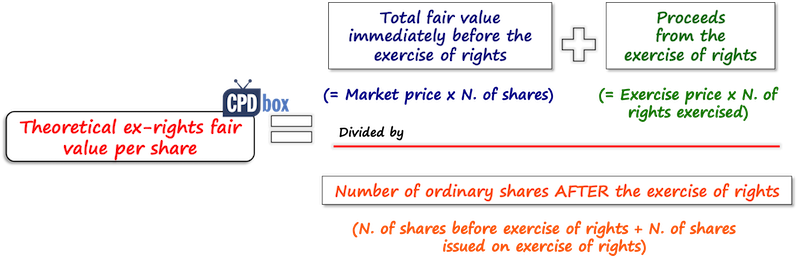

- Theoretical ex-rights fair value per share – this is the number that you calculate based on the following formula (in fact, you are calculating theoretical price per share as if the rights have already been exercised):

I know I know – this becomes really complicated, so let’s bring some order here and solve an example step by step with illustrating all these concepts.

Example: Earnings per share and rights issue

Question

On 1 March 20X1, the Company ABC offers all its ordinary shareholders the right to purchase ONE ordinary share for every FOUR ordinary shares that they hold, at 30% discount to the fair value (market price) – yes, you have seen this above.

Market price per share on 10 March 20X1 is CU 10 and this is the last day when the shares are traded with rights (not ex-rights).

ABC’s share capital consisted of 100 000 ordinary shares prior rights issue.

The last exercise date is 1 April 20X1 and all rights were exercised.

ABC’s profit attributable to ordinary shareholders was CU 200 000 in the year 20X0 and CU 250 000 in the year 20X1.

Calculate EPS with taking the rights issue into account. The end of the reporting period is always 31 December.

Solution

The points to remember:

- With the rights issue (or any issue with bonus element), you need to make a retrospective adjustment to both current period AND comparative period, too.

- You need to adjust BOTH basic AND diluted EPS (here, we have no indication of diluted EPS, so we will calculate just basic EPS).

Now let’s get to do the work.

As I promised above, let’s proceed step by step.

Step #1: Get your numerator – “E” or earnings

In this case, this one is easy, as we know the profit attributable to ordinary shareholders in each year:

- 20X0: CU 200 000;

- 20X1: CU 250 000.

CU is currency unit.

Step #2: Get your bonus factor

We need 2 numbers here:

- Fair value per share immediately before the exercise of rights – that is, on the last day of trading shares with rights: CU 10;

- Theoretical ex-rights fair value:

- Numerator:

- Aggregated fair value of shares immediately before exercise of rights – which is FV per share of CU 10; multiplied with the number of shares outstanding prior exercise of rights of 100 000 = and that is CU 1 000 000; PLUS

- Proceeds from the exercise of the rights, which is price of each new share issued of CU 10*70% (remember, they are issued with 30% discount); multiplied with the number of new shares issued = 100 000/4 = 25 000 (one new share per each 4 existing shares). Thus CU 7*25 000 = CU 175 000;

- Numerator is then CU 1 000 000 + CU 175 000 = CU 1 175 000;

- Denominator = Number of shares outstanding AFTER exercise of rights

- Number of shares outstanding BEFORE the exercise of rights = 100 000; PLUS

- Number of new shares issued = 100 000/4 = 25 000;

- Denominator is then 100 000 + 25 000 = 125 000.

- Theoretical ex-rights fair value = Numerator of CU 1 175 000 divided by denominator of 125 000 = 9,4.

- Numerator:

Our bonus factor is then CU 10 / CU 9.4 = 1,064.

Step #3: Get your denominator – “S” or weighted average number of ordinary shares

Here, we have two reporting periods to deal with:

Previous reporting period 20X0

The previous reporting period – year 20X0 – is very easy, because the rights issue happened in 20X1, not in 20X0.

And, it means, that we need to adjust the weighted average number of ordinary shares during the full year 20X0, because the full year 20X0 happened PRIOR rights issue.

The adjusted weighted average number of ordinary shares is calculated as:

- Weighted average number of ordinary shares outstanding in 20X0 of 100 000;

- Multiplied with bonus factor of 1,064…

…which gives us 106 400 shares.

Current reporting period 20X1

The things are slightly more complicated here, because the rights issue happened during the year – on 1 April 20X1, the last day of exercise of rights.

Therefore we will need to do some time apportioning, as shown in the following table:

| Dates | (A) Time proportion (N. of months/12) | (B) N. of shares | (C) Bonus factor | (D=B*C) Adjusted n. of shares | (E=A*D) Weighted average n. of shares |

| 1/1 – 31/3 | 3/12 | 100 000 | 1,064 | 106 400 | 26 600 |

| 1/4 – 31/12 | 9/12 | 125 000 | 1,000 | 125 000 | 93 750 |

| Total | 120 350 |

Note – you do NOT adjust the n. of shares with bonus factor AFTER the new shares from the rights issue were indeed issued. You adjust ONLY the periods before that.

Step #4: Calculate EPS

We have everything that we need now.

Let’s sum up the calculation in another table:

| Year | (A) Earnings – E (Step 1) | (B) WA Nr. of ordinary shares -S (Step 3) | (C = A/B) EPS |

| 20X0 | 200 000 | 106 400 | 1,880 |

| 20X1 | 250 000 | 120 350 | 2,077 |

DONE!!!

I really hope this was systematic, clear enough and brought some order into your thinking about this complication.

Any questions or ideas? Please leave me a comment below.

Thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

18 Comments

Leave a Reply

Hi Silvia,

Have you done an article to explain how to calculate diluted EPS when there is a convertible bond in place with time weighting factor?

Thanks for the article Ms.Silvia. But I have a clarification – When calculating the WANOS for Current reporting period 20X1 ,why is the date 1/1 – 31/3? the Right issue was issued on 1st March. Hence the Time proportion should be 2/12 right? Correct me If I’m wrong

hello Liz

As an attempted answer, 1st of march was the offer date and 1st of april was the exercise date. Hence the exercise rights is calculated after exercise NOT at the offer date

Hi Silvia. What would happen if a rights issue is made on the first day of the accounting year? Am I right in assuming that we do not apply the bonus fraction to the current year?

Thanks for the article. It was really very helpful.

i have been relieved of my misery 🙂 Thanks a million Silvia!

Hi Silvia, thanks for the articles and I would like to confirm that when the comparative figures are shown in the AFS, the basic EPS in the prior period should be based on 106,400 shares, right?

Thanks in advance!

I don’t know what you mean by AFS, but yes, as the article says – 106 400 shares in the comparative period.

Well articulated & explained. Thnx.

Hi Silvia. I just want to thank you for this. More power to your elbow

Dear Silvia, Hope my messages find you well..

Thank you for your great effort. Would you please tell me about of why we are using bonus factor to restating the Basic EPS of previous year, actually i really want to know with real life example. What would be happen if i do not restated last year Basic EPS for Right Issue. I want this answer from you in perspective of a company in Stock Exchange.

Hi Ahmed,

well, the example above is almost a real-life 🙂

We are restating it for 2 reasons:

1) This is what IAS 33 prescribes in paragraph A2 of the Application guidance (and IAS 33.28).

2) Rights issue is a combination of full-price issue and zero-price issue (“bonus issue”) because you are issuing the shares at discount. Hence you need to adjust previous periods to show the effect of zero-price issue on earnings per share in all presented periods.

If do not restate EPS in the previous years, then you are not showing comparable information to the investors.

also i will be appreciated if you give us an example for bonus issue and ex-right together.

please if you check the BPP book you will find that for current year he use another bonus Fraction.

and also i didn’t get what is bonus fraction effect in the number of shares. as per the example the shares number became 106400 instead of 125000 shares i really didn’t get this.

Hi Karim,

well I had to pull out my older BPP book since I am always using the formulas as stipulated by the standard rather than interpreted by some book – and I have the impression that in that book they used more-less the same calculation as I did.

The only difference is that they adjusted EPS for previous year by bonus fraction calculated as Theoretical ex-rights price / FV per share… and weighted average n. of shares for the current year by the bonus fraction calculated vice-versa as FV/Theoretical e-r price.

Well let me tell you that I prefer my approach since it is more consistent – you should ALWAYS adjust the weighted number of shares by the same fraction, in both years. Instead, they adjusted EPS by 1/bonus fraction in the previous year, and weighted average n. of shares by bonus fraction in the current year. Mathematically this is correct (because n. of shares is denominator in EPS), but for me it is less systematic and more messy. However it is up to you.

As for the number of shares – 106 400 shares is restated amount for previous year – the true amount was just 100 000 shares, because the new shares were issued in the current year, but we had to restate this amount by bonus fraction to 106 400. In the current year – please see the amount calculated in the table amount. In 20X2, if nothing happens, then the amount of shares will be 125 000.

In BPP book, they just restated EPS and used one amount of shares. Well again – not a systematic solution. You should remember to do the same thing in both years and not different things in these years.

However as I say – up to you. Good luck!

Thank you so much for your respond.

actually i agreed with you regarding to the bonus factor and BPP also use the same fraction in revision kit book.

my second question is why we restate by 106400 shares but in fact the shares became 125000. i understood how to calculate it but i need the logic on this.

Well, you restate only previous year 20X0 – then, the amount of shares was 100 000 only and you must show the effect of bonus element in the previous year, too – hence you restate it to 106 400.

In 20X1, you restate the amount of shares only prior issuing rights – that is for the first 3 months. Please revise the table above.

Dear Silvia, you are great and sharing your knowledge with others is a nice job. well done.